Colonial First State head of investments Scott Tully is a proponent of guiding disengaged default superannuation members into products with a risk profile appropriate to their stage in life. That belief informed the design of CFS’s MySuper product and is set to influence its approach to the incoming MyRetirement regime.

The 2011 Stronger Super reforms, which ushered in the MySuper licensing regime for default superannuation funds, gave providers the choice of either setting up a single balanced fund for all of their members or implementing a lifecycle fund model.

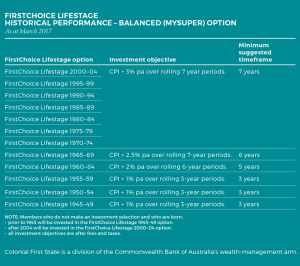

CFS was among the minority of providers that opted to offer a lifecycle-style MySuper product, which it called FirstChoice Lifestage.

This meant implementing 12 separate funds (segregated by age cohort), rather than a single fund for all default members. Properly identifying and transferring existing members into the right product was a mammoth administrative task, which CFS finally completed in June 2017, just shy of the July 1, 2017, deadline.

Tully, a big believer in the importance of structuring more tailored default products for these “typically disengaged” default members, is confident it was worth the extra effort.

“In the short term, it would have been much easier to just stick everything in a balanced fund; but long term, we think it is much better for members to have this differentiation.”

He is “fairly confident” the lifecycle approach has already proven its worth.

Since inception, the FirstChoice Lifestage portfolios have consistently beaten their targets.

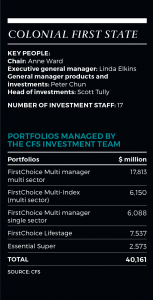

CFS is a division of the Commonwealth Bank of Australia’s wealth-management arm. It sources roughly one third of its asset-management services from related party Colonial First State Global Asset Management, but operates separately.

Tully’s 17-person internal team is responsible for the management of the FirstChoice multimanager, multi-index and Lifestage portfolios, as well as Commonwealth Bank Essential Super (a public offer Lifestage product marketed

to employers looking for a default fund for their staff).

Overall, CFS has $40.2 billion in funds under management. The bulk of that, roughly $30 billion, is across products offered through the retail platform business. Clients in the multimanager and multi-index platform products are typically over 50 and have seen a financial adviser, while clients in the default MySuper options – First Choice Lifestage and Commonwealth Bank Essential Super – tend to be younger and not advised.

Factor investing

While the investment operations staff at CFS have been focused on finalising MySuper compliance, the investment management team have been spending much time researching new factor-based investment strategies.

While the investment operations staff at CFS have been focused on finalising MySuper compliance, the investment management team have been spending much time researching new factor-based investment strategies.

Since FirstChoice Lifestage portfolios were created in 2013, the entire equities component has been deployed according to factor-based strategies. Tully describes the philosophy behind his approach to factor-based investing as, “the idea that you can get active returns by decomposing a particular sector into different drivers of return”.

Originally, the entire equities portfolio was managed with a value factor strategy run by CBA-owned quantitative manager Realindex Investments. Over the last 18 months, changes have been made to start diversifying the equities factor exposures.

“The very strong value skew in Lifestage was a bit of a negative at the end of 2015, but into 2016 it was a very strong addition to our return,” Tully says. “So, what we have done is reduced some of that value skew and brought in managers with a low-volatility approach.”

Tully says the degree to which the skew to value has been reduced varies across the different age cohorts.

“For our younger members, value has been a good contributor of return; whereas if you’re an older member, you probably don’t want to have a large exposure to value because it does tend to take a little while for that factor to play through.”

Tully and his team are now turning their attention to determining what other factors should be introduced to the FirstChoice Lifestage portfolios – such as momentum or small caps. They are also reviewing a number of multifactor strategies. Once these strategic decisions have been made, Tully won’t be sitting on his hands too long trying to time

the entry point.

“If you think it is something that should be done in a portfolio, then you can finesse the timing a little bit but, primarily, you are looking to make that allocation, because we are investing long term.”

Tough outlook

Tough outlook

Tully got his start in the investment management industry in 1995 as an analyst and manager at Colonial State Bank, before it was bought out by CBA. Prior to that, he spent five years working as an actuarial analyst, having begun his career with Mercer. Back in 1989, when he joined the industry, the official Reserve Bank cash rate peaked at 18 per cent.

The outlook for rate moves over the next 25 to 30 years is entirely different, from a starting point of 1.5 per cent.

An obvious implication is that superannuation managers, including CFS, will struggle to deliver returns in line with historical averages.

“One of the big questions is, ‘Where do interest rates go from here?’… But we are not trying to make that call,” Tully says. “We have progressively taken money out of bonds over the last three to four years and allocated to less duration-sensitive assets. We still believe there is a space for bonds in a portfolio, we just don’t have as [many] as we did once upon a time.”

Tully is also looking to allocate more capital in absolute-return strategies, across both equities and bonds. In recent years, CFS has allocated away from developed market shares and bonds into emerging markets and more alternative asset classes, such as global infrastructure and real-estate trusts. Tully expects this trend to continue and that these assets will be essential to generate the returns required to continue paying out large income streams to retirees.

Modernising pensions

CFS is the second-largest payer of pensions in the country, behind only the federal government. In the last 12 months, the organisation has distributed $3 billion in private pensions to 165,000 retirees.

In principle, Tully supports the government’s effort to nudge super funds into offering a Comprehensive Income Product for Retirement (CIPR) as an alternative to a lump sum or account-based pension.

He thinks the new breed of retirement accounts, which the government has moved to re-badge as MyRetirement products, will help the bulk of Australians, who retire neither poor nor rich.

“For members with low balances, the age pension will always be the primary source of income, while at the other end of the spectrum, there are people who hit or come close to the $1.6 million transfer balance cap and talk to an adviser about how to structure their assets in a way that makes sense,” he says. “It is those people in the middle – who will have a reasonable sum accrued but have less access to the age pension, need some help and may not have an adviser – that the government is trying to help with CIPRs.”

Tully sees “lots of work” to do on Treasury’s draft CIPR framework. “But I am confident that, with industry input, a solution will be found.”

This article first appeared in the July 2017 print edition of Investment Magazine. To subscribe and have the magazine delivered CLICK HERE. To sign-up for our free regular email newsletters CLICK HERE.

Leave a Comment

You must be logged in to post a comment.