An obsession with peer-relative benchmarking and a gross failure to build trusted engagement with members is endangering the Australian superannuation industry’s social licence to operate, argues Sean Henaghan, the chief investment officer and director of AMP Capital’s multi-asset group.

Henaghan spoke to Investment Magazine about how his team is structured to eschew the peer-relative mindset in favour of a focus on meeting absolute targets, and how the industry must evolve to shore up trust.

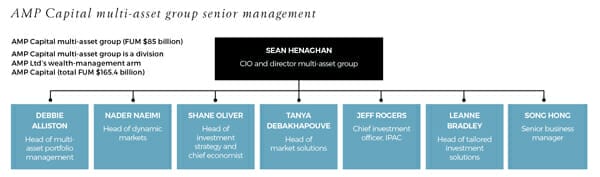

AMP Capital, which is the wealth-management arm of ASX-listed financial services giant AMP Ltd, has a total of

$165.4 billion in funds under management. The multi-asset group that Henaghan heads up is responsible for $85 billion of that.

Seven senior executives report directly to Henaghan, including well-known media commentators AMP Capital’s head of investment strategy and chief economist Shane Oliver, and head of dynamic markets Nader Naeimi. However, it is the multi-asset portfolio management team, headed by the more low-profile Debbie Alliston, that Henaghan describes as the “key source of competitive advantage” in the business.

Alliston’s team has ultimate accountability for the performance of nearly all of the 45 funds in the broader multi-asset group, including a number of smaller corporate super funds that remain as a legacy of AMP’s troubled takeover of AXA Asia Pacific six years ago. While most of the funds are still peer relative, the new generation of AMP Capital funds is not, reflecting Henaghan’s belief the industry needs to shift away from benchmarking against strategic asset allocation and are instead manage portfolios to specific client goals. This type of multi-asset approach is quite rare within the Australian institutional asset management industry.

“Our industry has always acted like picking the manager is the most important thing, but manager selection is just icing on the cake,” Henaghan says. “The most important decision we need to make is which idea or which market to invest in…How we then invest in that theme or market is second order.”

Henaghan says the industry is endangering Australians’ compulsory retirement savings by clinging to its index and peer-relative benchmarks. To illustrate the problem, he recalls how AMP Capital (like the industry at large) failed to meet its objectives during the global financial crisis in 2007.

“Everybody knew equities were overvalued,” Henaghan recalls. “We’d scaled back our active risk compared to the peer group…but we still went over the cliff with everyone else.”

He fears the prevalent attitude that losing other people’s money is OK so long as a fund still outperforms its benchmarks will spell disaster in the next major market crisis, prompting another exodus out of large-scale, sophisticated, pooled-funds and into self-managed super funds.

“What happens after something like the GFC is the member says, ‘Bugger you, I’m not paying 100 basis points to lose my money. I’m going to set up an SMSF myself,’ ” he says. “Well, the average SMSF has 40 per cent in Aussie banks and high-yielding stocks, 40 per cent in cash, and 20 per cent in international stocks and property. That’s a shocking portfolio and people are doing that because we as an industry have failed them.”

Henaghan’s former boss, David Kiddie, who held the title AMP Capital CIO and head of the multi-asset group and specialised investment teams from 2009 to 2014, instigated the organisation’s reshuffle into its current multi-asset approach in the wake of the GFC.

Case for lifecycle products

Compatible with the philosophy of running funds without reference to a strategic asset allocation, AMP Capital’s default MySuper option is a lifecycle product, rather than the typical one-size-fits-all balanced fund approach.

Henaghan uses a river-crossing metaphor to expound on why the lifecycle approach to default, where asset allocation is actively managed along a glide path as members approach retirement, is a “more fit for purpose” model than running a single balanced fund.

“Imagine you are trying to help a bunch of people cross a river that on average is [a metre] deep, but there are pockets that are [2 or 3 metres deep]. Under your balanced fund scenario, 20 per cent of your members are going to drown. But hey, that’s OK because on average we did OK. No. We want to manage that sequencing risk to get everyone across the river.”

One of the next projects for AMP Capital will be to develop a comprehensive income product for retirement (CIPR) to offer as a default option to retiring default members, as a complement to the lifecycle funds. Ultimately, Henaghan would like to develop a cradle-to-grave solution.

Retirement solutions

Henaghan is “deeply disturbed” by the trend for retirees to favour passive, conservative funds in the current low-yielding market. What retirees need is a portfolio designed to specifically target volatility, income, inflation and longevity risk, he says.

The missing building block at the moment is the ability to manage for longevity risk, but Henaghan is hopeful that having made deferred annuities legal from July 1, 2017, the government will pursue further reforms to make them more compatible with the age pension asset test.

He says that, along with offering retirees better products, the industry also needs to do a better job of communicating with superannuants as they approach retirement, so they are better prepared.

“Telling members they’ve got a $100,000 balance is a wealth fallacy,” says Henaghan, who is an advocate for providing retirement income projections, rather than just account balances, on statements.

Canary in the coal mine

With a history as one of the first big pension managers in Australia, AMP’s superannuation business has been under pressure in recent years as its client base has aged and started drawing pensions without a corresponding uptick in new

young members, leading to net outflows.

Henaghan doesn’t sugar-coat the challenge that presents to the business.

“Absolutely that [net outflow] is a problem. That is telling us something. It is telling us that we are not relevant,” he says. “This is serious.”

A challenging macro-economic environment also means the outlook for average investment returns over the next decade or so is set to be significantly lower than consumers have grown accustomed to over the past decade, since the GFC. This raises the risk of waning public support for compulsory superannuation if the system can’t keep delivering results.

“I think there is a big risk to mandated super, because people somehow think managing money is easy and I think that is partly because we haven’t effectively communicated what it is we do,” Henaghan says.

Radical transparency

In order to forge stronger engagement with consumers, the industry needs to push itself to become more transparent, Henaghan says.

He lambastes those who have opposed incoming regulations to force all institutional investment managers to be far more transparent about their portfolio holdings on the grounds it would compromise their intellectual property (IP).

“How arrogant,” he exclaims. “Anyone who reckons the rest of the industry would be just waiting to see their holdings to copy them is just kidding themselves.”

He thinks the new rules, which were recently delayed for two years amid fierce opposition from the industry, are “brilliant” and plans to ensure his team is complying with them before the end of 2017.

Henaghan predicts that as consumers become more digitally savvy they will demand more information about how their money is invested, rejecting institutions that refuse to provide it.

Plus, he argues it is an outdated notion for funds to think about their IP as residing in their research or investment records.

“When I started in the industry 30 years ago, the theory went that your IP was only valuable if you protected it,” he explains. “Well the world has changed and now your IP is most valuable if you share it. Your real IP is in your people, not in the stocks in your portfolio.”

Building an IP network

In line with this, Henaghan wants to create an “IP network” based on building deeper relationships with other asset owners and managers.

He credits Schroders, Wellington Management, T. Rowe Price, JP Morgan Asset Management and PIMCO as examples of global funds management firms that take an open approach to sharing IP with their clients.

AMP Capital also shares IP with Australia’s $148 billion Future Fund. The sovereign wealth fund’s chief executive, David Neal, and Henaghan are old mates, having worked together at Watson Wyatt, where Neal rose to head of investment consulting.

The personal connection helped set the stage for the collaboration, but it also helps that the two organisations are not in competition and share a multi-asset approach.

Members of the investment teams from the two organisations meet to discuss their latest strategic thinking about everything from investment theory to front-office technology projects.

Henaghan finishes our interview by offering an “open invitation” to any other funds that want to get together and talk.

This article first appeared in the August 2017 print edition of Investment Magazine. To subscribe and have the magazine delivered CLICK HERE. To sign-up for our free regular email newsletters CLICK HERE.

Leave a Comment

You must be logged in to post a comment.