Over the last three years, Mine Super has worked hard to establish the foundations for future investment excellence. We have internalised strategic asset allocation and updated the investment operations platform. We can already see the results of this endeavour – our portfolios are constructed better.

Now comes the exciting part.

We’re changing the way two of our existing internal teams work, to get the most out of the other upgrades. It’s the final piece of this process and it’s what will ensure that the investment team makes the most of the platform we’ve established.

To tap into this upside, we must better integrate our existing manager research and asset allocation teams’ activities. Members of both teams need to partially adopt an investment strategist mindset and live our whole-of-portfolio focus.

For those involved, this is exciting on many levels – collaboration, interest, contribution to outcomes, and career development.

At Mine Super (formerly Mine Wealth + Wellbeing), manager researchers now have input into many of the strategic asset allocation assumptions and are constantly challenged to bring new investment ideas to the table. From here, they work with asset allocation to research the opportunity, bring it into our strategic asset allocation (SAA) framework, and see if it will improve our portfolios.

Similarly, the role of the asset allocation team is broader than maintaining and improving existing processes. These team members are challenged to have the curiosity to learn constantly about new investment opportunities, and work with the researchers to bring them into our SAA framework.

Even more improvements will come in this final stage of a three-step transformation. But before we could get to this point, we had to lay the ground work. Here’s how it was done.

Step 1: Internalising strategic asset allocation

We view the SAA as the foundation of excellent portfolios. The big question was whether investment excellence could be achieved if you outsourced your SAA to a consultant. While we regard the work of consultants highly, their advice can only ever approximate a solution to the problem of capturing the opportunities available to us within the constraints we face.

Insourcing SAA is not easy. Developing the ability to at least match the quality of the services our asset consultant provided took a long time. We also had to provide our investment committee members with insight into what we developed so they could sign off on an internalised model with conviction. We had two consultants come in and review our models and processes and present to our IC. The IC approved the switch to our internal SAA framework in April 2016.

There are many advantages gained from internalising SAA:

• Establishing a culture of asset ownership by owning the return, risk, and diversification assumptions of each asset sitting in your portfolio

• Accountability for the science of forecasting and portfolio construction. There are many competing methodologies and techniques

• The ability to model each asset in the portfolio, rather than generic asset classes. This is particularly relevant to private assets, where there can be significant dispersion among individual assets within the same broad category

• Incorporation of assumptions around active returns and fees.

Once the SAA process is internalised, there is the chance for further improvement and development. It becomes part of the investment team’s DNA.

Step 2: Rebuilding the investment operations platform

Once Mine Super internalised its SAA, it found that it was operationally constrained from implementing its targeted portfolios. Owning the SAA capability allowed the fund to calculate the expected opportunity cost of this constraint, which then informed the business case for rebuilding the investment operating platform.

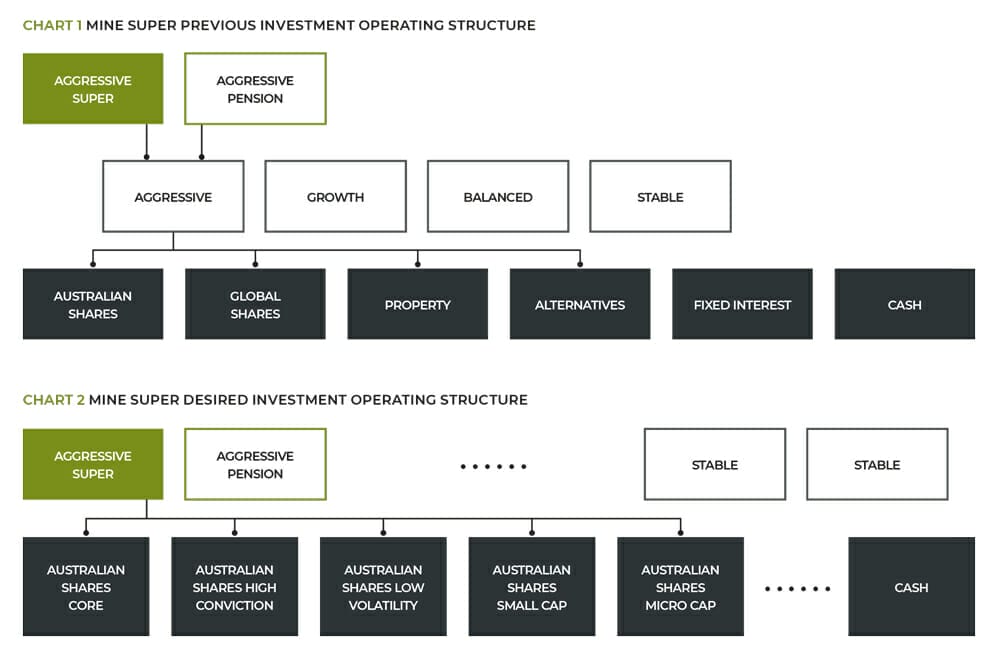

The previous investment operating structure of Mine Super, like that in many super funds, is detailed in the accompanying diagram.

We identified weaknesses in this structure: each diversified option could allocate only to six asset-class sectors. We believe that, optimally, our various diversified options would target different opportunities within sectors. The greatest constraint was having a single alternatives pool, an area where a range of high- and low-risk opportunities exist.

The super and pension versions of each diversified option were both simply feeders off the respective diversified option pool. We weren’t accounting for the different tax environments our members faced.

Our desired operating structure was: a large, unconstrained number of sectors (now about 40 active sectors). The portfolios for the super and pension versions of each diversified option are unique in their sector mix.

The benefits of this structure are significant: the operational ability to implement the portfolios our SAA process identified. We have made greater use of the opportunities within alternatives as we seek to diversify equity beta among higher-risk portfolios, while replacing fixed interest exposures in lower-risk portfolios.

There are unique super and pension portfolios for each of our diversified options, accompanied by unique investment objectives. We account for the different tax environments that can affect both return and risk expectations (we model different tax environments in our SAA framework).

The project took more than six months to implement. There was collaboration both within Mine Super (among the investments, finance, governance and risk teams, and the project office), and with external service providers (most notably custodian J.P. Morgan, transition manager Citi, and currency overlay manager State Street Global Advisors). Mine Super successfully rolled onto the new investment operating platform on July 1, 2017.

David Bell is chief investment officer of Mine Super.

Leave a Comment

You must be logged in to post a comment.