Spare a thought for the directors of Glencore, one of the world’s largest thermal coal producers and traders, who must be a little confused by all the free advice – and admonishment – they have been recently receiving.

The Australian Centre for Corporate Responsibility (ACCR) accuses the company of placing a “reckless bet” against the energy transition by not aligning its coal production plans with the IEA’s Net Zero Emissions (NZE) scenarios.

At the same time, the Institute for Energy Economics and Financial Analysis (IEEFA) is urging the Glencore board not to proceed with a demerger of its coal assets because it fears they will become owned by less responsible investors with less commitment than Glencore to reducing emissions.

Meanwhile, Tribeca Investment Partners is recommending Glencore shift its primary listing from the London Stock Exchange (LSE) to the Australian Securities Exchange (ASX) where Australia’s “more pragmatic” superannuation funds are likely to be very big buyers of its shares.

However, Australia’s second largest super fund Australian Retirement Trust (ART) has just announced it is excluding direct investment in thermal coal companies.

Swiss-based Glencore holds its annual meeting at the picturesque Theater Casino Zug on 29 May and it will be fascinating to see how the board addresses these matters.

At the heart of things is Glencore’s current acquisition of a 77 per cent interest in Canadian company Teck’s steelmaking (metallurgical) coal business Elk Valley Resources for US$6.93 billion ($10.5 billion).

When the deal was announced, Glencore said it planned to spin off the combined coal assets into a new company that would be listed on the New York Stock Exchange (NYSE).

This would leave Glencore as a diversified commodities group with strong exposure to copper and other metals needed for the energy transition.

ESG 3.0

Glencore’s situation presents some interesting scenarios, and, regardless of whether Glencore takes Tribeca’s advice, it raises some interesting questions about the Australian super fund appetite for thermal coal.

“Retention and responsible depletion of fossil fuel assets are at the frontier of environmental governance. We see this as being the view of industry leaders, political commentators and asset managers alike,” Tribeca says in a letter to Glencore.

Tribeca believes there is a “shift away from rudimentary ‘ESG 1.0’ strategies and towards more pragmatic ‘ESG 3.0’ investment policies” that are more focused on transition than divestment.

This shift is occurring in Australia but in Europe fossil fuel producers are still “demonised” according to Tribeca. ASX investors – who Tribeca says have “an increasingly pragmatic stance” – place much higher valuations on coal stocks than LSE investors.

Tribeca calculates that – all else being equal – transferring from the LSE to ASX would add US$13 billion ($19.6 billion) to Glencore’s market capitalisation.

This is based on some rather bold assumptions, including that Australian institutional investors “will seek to occupy 35 per cent of the Glencore register” if the company were to move to the ASX. This would require super funds forking out tens of billions of dollars to buy Glencore shares.

Tribeca believes Australian super funds are starved of opportunities to invest in the energy transition and would love to buy Glencore because of the exposure it offers to copper and other metals.

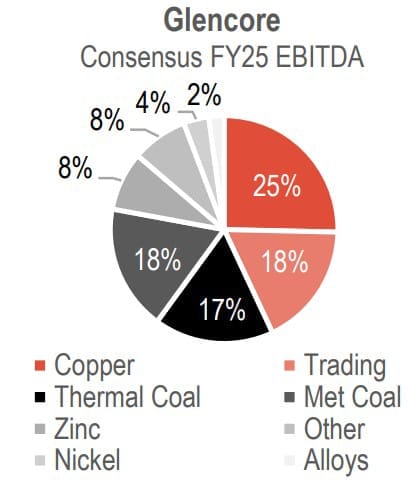

Tribeca thinks Australian asset owners and managers would be happy to buy Glencore shares even if an estimated 17 per cent of its earnings (see pie chart) will come from thermal coal in 2025 (not to mention another 18 per cent from metallurgical coal).

The ART of exclusion

But one asset owner who presumably wouldn’t be a Glencore buyer is Australia’s second-largest super fund ART, which not long after Tribeca’s letter put thermal coal on its investment exclusion list.

ART is excluding direct investment in Australian and international shares of companies generating more than 10 per cent of gross revenue from the mining and sale of thermal coal.

However, if Glencore were to hold onto its coal assets but continue its diversification into energy transition metals, it might in a few years be deriving less than 10 per cent of its revenue from thermal coal.

This would mean ART would then be free to invest in a company that may still be the world’s largest thermal coal exporter but would still be screening out much smaller thermal coal producers that are responsible for much lower absolute emissions.

Soul Patts

One big investor that may be happy to buy Glencore is ASX’s Top 50 investment company, Washington H. Soul Pattinson.

Soul Patts owns 39.24 per cent of ASX-listed New Hope Coal and 19.9 per cent of ASX-listed Malabar Coal (both of which have thermal coal expansion plans in Australia).

As part of its rapidly growing private credit activities, Soul Patts also recently helped finance major coal acquisitions by two other ASX-listed groups – Stanmore Resources and Whitehaven Coal – and thus helped fill the funding gap left by super funds and banks pressured into exiting this space.

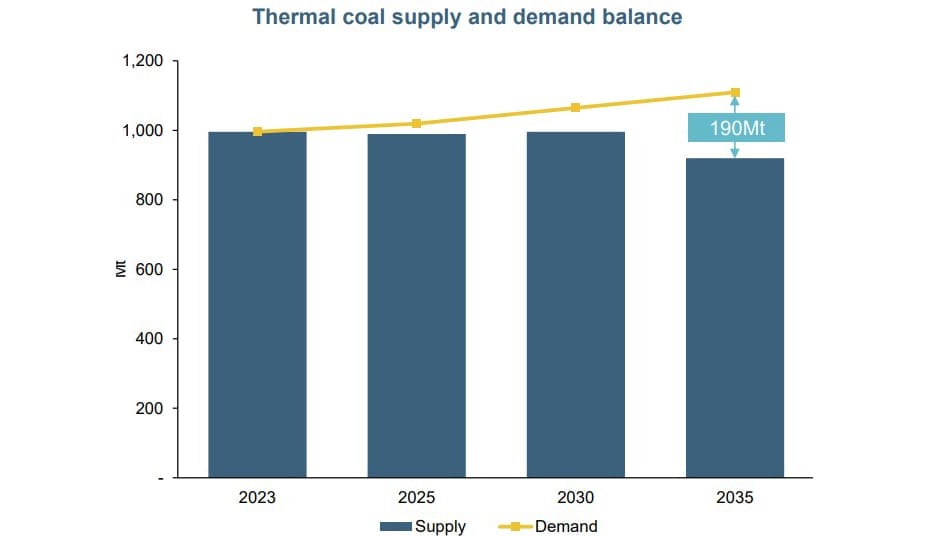

New Hope believes the “fundamentals for global seaborne thermal coal look increasingly attractive, especially for Australia’s low-emission, high-quality coal” (see graph above).

In a recent interview New Hope CEO Rob Bishop said he believed the world will continue to need thermal coal for decades into the future.

Glencore agrees, saying if carbon capture technologies do not sufficiently advance (which they are very unlikely to) it sees a “role for unabated thermal coal for electricity generation beyond 2040”.

Soul Patts likes to highlight its “unconstrained mandate” to invest in any sized business in any industry.

With its big cross-shareholding with ASX-listed Brickworks and some other friendly shareholders, Soul Patts doesn’t need to pay much attention to any activist ESG shareholders who want some constraints.

Interestingly, a couple of years ago New Hope accused super funds of buying small quantities of its shares for the purpose of quickly selling them to gain ESG kudos.

“We have seen superannuation funds and major investment firms take a small position in the company only to sell the shares in a very public announcement to create the perception of being a responsible investor,” New Hope said.

Reckless?

ACCR says Glencore’s “persistent unresponsiveness” on its climate disclosures demonstrates a “governance failure” and ACCR intends to vote against the company’s 2024-26 Climate Action Plan (CATP) – and the Glencore chair – at the 29 May AGM.

ACCR says the CATP “fails to demonstrate how Glencore will responsibly wind down its thermal coal production”.

Glencore has “dropped its coal production cap, right when it might be needed most and introduced a new 2030 emissions target that allows for less action between 2026 and 2030 than in the previous climate plan.

“To have the world’s largest thermal coal exporter effectively walking away from Paris alignment is an enormous risk to Glencore’s investors and a risk to all portfolios exposed to the systemic risks of climate change. It represents a reckless bet against an orderly and timely energy transition,” according to ACCR.

Responsible?

Tribeca, however, views Glencore rather differently, making the surprising claim that “Glencore’s responsible stewardship of its coal portfolio is at the frontier of sustainability”. It says the company’s strategy “optimally balances ecological, social, and economic outcomes”.

Tribeca says “the cashflow generated from its production of traditional energy sources is invested in future facing commodities such as copper, making Glencore one of the most efficient intermediaries in the energy transition”.

IEEA also seems happy to stick with the devil you know, saying “investors have increasing concerns about how responsible it is to divest coal mine operations given the lack of any emissions impact such a move would have”.

On Glencore’s coal demerger plans, IEEA says, “emissions may actually rise if the new owners seek to increase output. In addition, investors may not be keen to lose the cashflows that result when coal prices are high, which could be reinvested in commodities with a brighter long-term future.

“Investors increasingly have policies barring them from holding shares in pure-play coal companies, and some may prefer diversified miners like Glencore to keep their coal operations, so they can maintain their exposure to coal”.

So, have some ESG-conscious investors been getting it all wrong? Does the world, in fact, need thermal coal profits in order to help fund clean energy transition?

Leave a Comment

You must be logged in to post a comment.