Gabon’s transitional president, General Brice Clotaire Oligui Nguema, last month visited ASX-listed Genmin’s Baniaka iron ore project in the African nation’s Haut-Ogooué province.

During the visit (pictured) Genmin said General Nguema – who led last year’s coup ousting President Ali Bongo, whose family had ruled the country for more than five decades – “encouraged the company to develop Baniaka as quickly as possible”.

The company’s goal is to “sustainably produce a suite of greener, higher value iron ore products at Baniaka that are recognised internationally through brand identification”, and to this end, it recently registered the Baniaka Green trademark.

Genmin is one of a growing number of project proponents around the world promoting “green iron ore” or “green iron” projects they say will help decarbonise the global steel industry supply chain over the coming decades.

It seems nearly every iron ore-related project in the world – including those in Australia currently seeking tens of billions of dollars in investment capital – now claims some sort of green credentials.

This is problematic as there are no agreed definitions for “green iron ore”, “green iron” or “green steel” and because – as will be discussed – green comes in many different shades, some of which make only small contributions to steel decarbonisation.

Hematite verses magnetite

But first some scene setting. Australia may be the world’s largest iron ore producer and exporter and host the world’s largest iron ore resources but the emerging desire for “green iron” poses a threat to its long-time dominance in this sector.

The global steel supply chain is responsible for about 8 to 10 per cent of the world’s CO2 emissions, mainly from the burning of metallurgical (coking) coal by steelmakers during the iron-making process.

Nearly all the iron ore Australia digs up and ships to steel makers is hematite. However, this hematite is currently not suitable feedstock for the next generation of low-carbon electric arc furnaces (EAFs) that over time will replace coal-consuming blast furnaces.

Magnetite ore is considered a better feedstock for green iron technologies such as direct reduced iron (DRI). Magnetite ore is lower grade than hematite but can be upgraded using existing technologies. And its magnetic properties mean impurities can also be more easily removed.

Australia boasts vast resources of magnetite (in Western Australia and South Australia) but these have largely stayed in the ground because Australia’s biggest producers, BHP and Rio Tinto, have for decades been content to accept large profit margins from simply digging and shipping hematite.

Green iron hubs

So here lies the big opportunity – and the big challenge. The opportunity is developing “green iron hubs” where projects are run on renewable energy and use green hydrogen (instead of coal) to make DRI or hot briquetted iron (HBI) that is then exported to steel mills.

Australia can grab this opportunity in a couple of ways. We can pivot to more magnetite projects in order to compete with the growing global pipeline of projects and/or we can develop technologies that will enable our hematite to be used for DRI/HBI.

As part of its Green Iron and Steel Strategy, South Australia – which has large magnetite resources – has issued an expression of interest call seeking partners to jointly investigate the development of a green iron industry by 2030.

Western Australia has similar green iron ambitions but given the state is the world’s biggest hematite producer, it wants both hematite and magnetite to be part of steel’s decarbonised future.

The Australasian Centre for Corporate Responsibility (ACCR) predicts the pursuit of zero emissions steel production will lead to a fundamental change in the steel value chain.

ACCR’s Forging pathways report expects “a shift where the ironmaking and steelmaking process is decoupled, with green iron production occurring where there is significant renewable energy potential, either close to iron ore mines or within a reasonable distance for transport. The resulting green iron can then be moved to locations where green steel is manufactured”.

Situating green hydrogen production at the point of iron reduction gets around the complexities associated with shipping hydrogen.

WWF Australia’s Australia’s Green Iron Key report agrees, saying “instead of renewable hydrogen export, the logical approach is to embed the emissions reduction capability of renewable hydrogen in new export products, including green iron”.

Shades of green

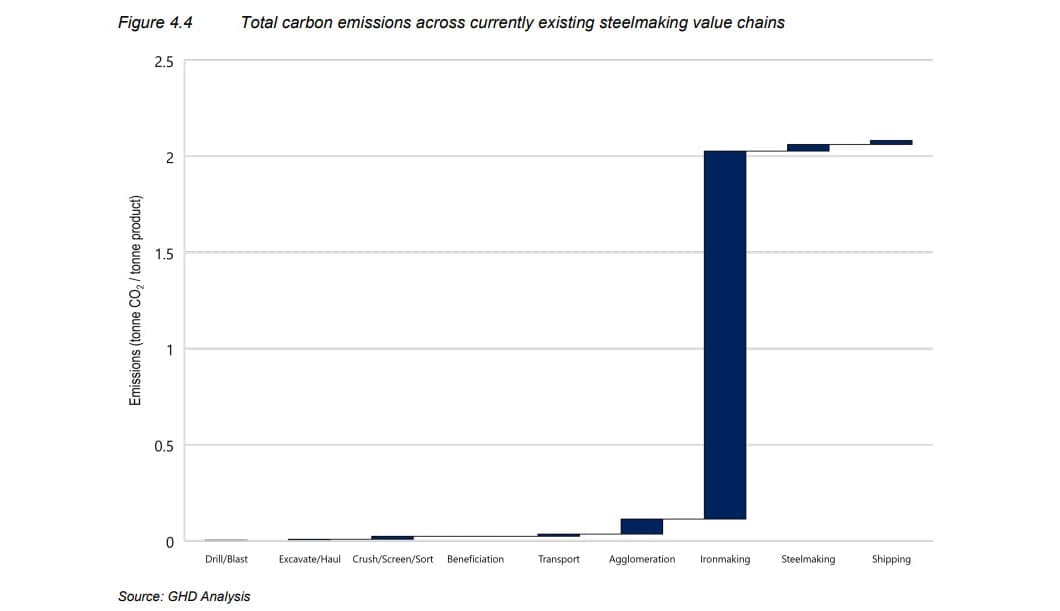

One way asset owners and managers can assess the green credentials of a project is to take a close look at the degree to which a project directly contributes to reducing emissions in the steel production supply chain. The waterfall chart below is helpful here.

A company may say it has a “green iron ore” project if an existing or a new mine will be run on renewable energy instead of fossil fuels (as is the case with the Banaika project, which will be powered by the nearby Grand Poubara Hydropower Station); it beneficiates (improves) its ore through a green process; or it is using renewable/alternative fuels for transport.

However, as illustrated by the chart, all these activities can only marginally reduce emissions in the steelmaking value chain.

A project becomes a “green iron” one if it plans to produce and export iron ore pellets using green hydrogen (i.e. hydrogen produced with renewable energy). Here, magnetite concentrates are better suited than hematite fines to turn into “green pellets”.

To eliminate emissions from the agglomeration stage in the chart, green hydrogen replaces gas heating in the pelletising facilities. Unfortunately, hydrogen costs are currently too high for a green pellet project to compete against the fossil fuel process.

As the chart also shows, it is the iron-making process that is by far the most carbon-intensive part of steel making, so this is where ESG-focussed and/or climate-conscious asset owners and managers will potentially get the most bang for their buck.

The Holy Grail is producing green HBI from green pellets, using renewable hydrogen as a reductant. Currently, every tonne of iron produces about 1.7 tonnes of CO2. However, green hydrogen can replace coke and gas for ironmaking, eliminating emissions from the most carbon-intensive stage of steel-making.

But again, the high cost and lack of availability of green hydrogen means such facilities are a long way off. So many green iron projects are likely to initially have shaft furnaces running on gas, with the promise of transitioning to hydrogen feedstock over time.

Scope of activism

Interestingly, while reducing overall emissions from ironmaking this approach would initially ‘onshore’ Scope 3 emissions, turning them into direct Scope 1 emissions for Australian green iron projects.

While new steelmaking technologies may develop to make green steel from current hematite direct shipping ores, “if this technology is delayed then this scenario becomes more likely,” MRIWA says.

No doubt this scenario will be used by BHP, Rio and Fortescue (which, by the way, is also now producing iron ore in Gabon) to argue for generous green iron production credits that may be on offer under the Commonwealth Government’s Future Made in Australia Act.

However, it is arguable whether taxpayers should have to come to the rescue. BHP and Rio have long promised they would value-add to Australia’s iron resources and not just dig and ship. Now it seems their recalcitrance might catch up with them.

BHP, Rio and Fortescue (which last month backtracked on its broader green hydrogen ambitions) say they are all investigating options to make their Pilbara ores suitable for a DRI-EAF route, or to advance alternative iron and steel-making processes that can utilise lower-grade hematite ores.

Asset owners and managers would, however, be well-advised to regularly question the Big 3 and other green iron proponents on exactly what progress is being made on their initiatives and their level of commitment to them.

It was in March this year that Rio announced – following engagement with ACCR, the Australian Council of Superannuation Investors (ACSI) and Fidelity International – it was committed to enhanced disclosure on its plans to reduce scope 3 emissions from the processing of its iron ore and would “continue its enhanced approach to climate advocacy”.

But late last month ACCR suddenly cut engagement with Rio after discovering the company had been involved in what ACCR described as “negative advocacy” regarding the government’s Nature Positive Plan.

ACCR said it was “stepping away from an agreement to support climate and decarbonisation related engagement with Rio Tinto. We will not participate in engagements that could rightly be perceived as greenwashing”.

Leave a Comment

You must be logged in to post a comment.