Published in partnership with Northern Trust Asset Management.

China’s weight among emerging markets equities has risen significantly since the Global Financial Crisis in 2008, peaking at about 40 per cent. Investors are looking for ways to manage the risk of this outsized weight, or even remove Chinese equities, without significantly affecting performance. We analyse China’s impact on emerging markets and global indexes, and we propose how investors may seek to control China’s influence in their emerging markets equity allocation.

China remains a relatively small piece of the global market, at 3 per cent of the global MSCI ACWI IMI Index. To put that in perspective, Apple represented about 4 per cent of ACWI IMI as of June 30, 2023. Removing China from the global portfolio is akin to choosing not to hold the tech giant. While this may not seem significant, it does introduce meaningful tracking error for passive investors relative to global benchmarks.

Index performance with and without China

We compared the performance of the emerging markets and global equity indexes with China and without China over the most recent five-year period and found that:

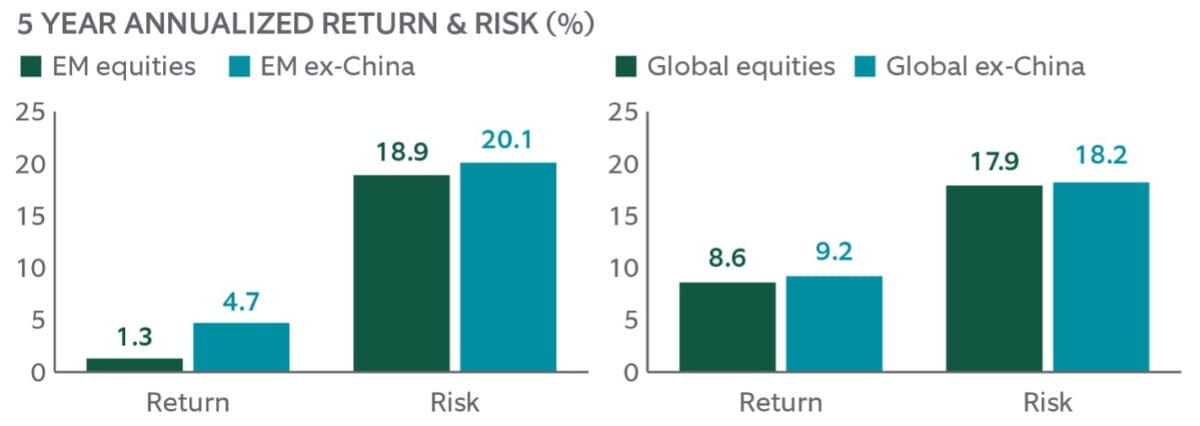

- The MSCI Emerging Markets Index returned 1.3 per cent annually with volatility, as measured by standard deviation, of 18.9 per cent. Removing China would have led to a 3.4 per cent higher annualised return with just a 1.2 per cent higher risk.

- At the global level, the differences are less pronounced. The MSCI ACWI IMI Index returned 8.6 per cent annually with a risk level of 17.9 per cent. Removing China increased the return by 0.6 per cent and risk by 0.3 per cent.

- Notably, the indexes without China outperformed because of China’s underperformance during the period as the country’s economy struggled to recover from the pandemic.

Source: Northern Trust Asset Management, Bloomberg. Risk is standard deviation. EM = MSCI Emerging Markets Index. Data from June 30, 2018 through June 30, 2023. See disclosure at the end of the report for indexes used. Past performance is not indicative or a guarantee of future results. Index performance returns do not reflect any management fees, transaction costs or expenses. It is not possible to invest directly in any index. Indexes are the property of their respective owners, all rights reserved.

For a more sophisticated view, we examined China’s exclusion from the angles of tracking error, periods of stress and geographic profile.

China’s impact on tracking error

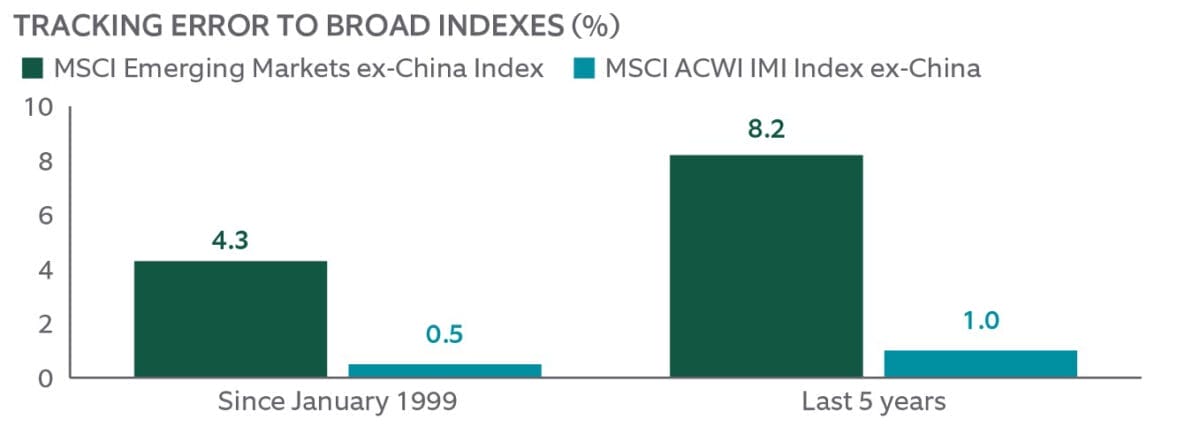

To demonstrate how much the index’s performance without China differs from the index that includes China, we examined historical tracking error, or the percentage that the MSCI Emerging Markets ex-China Index differed from the broader MSCI Emerging Markets Index over the last five years.

The data suggests that, in any given year, an ex-China emerging markets investment is likely to outperform or underperform the MSCI Emerging Markets Index by as much as 8.2 per cent – a significant number. However, at the global equity portfolio level, removing China becomes much less noticeable, with a historical tracking error of just 1.0 per cent. This number, although smaller, is still significant for tracking-error-conscious investors whose investment policies may stipulate MSCI ACWI IMI as the benchmark.

EXHIBIT 2

Source: Northern Trust Asset Management, Morningstar. Historical trends are not predictive of future results. See disclosure at the end of the report for indexes used. Data is as of June 30, 2023. Since inception data is from December 31, 1998, to June 30, 2023. The broad indexes are the MSCI Emerging Markets Index for the MSCI Emerging Markets ex-China Index and the MSCI ACWI IMI Index for the MSCI ACWI ex-China IMI Index. Tracking error measures the standard deviation of the difference between the investment performance of the strategy or fund and that of the Index. There is no guarantee that tracking error targets can be achieved; actual or experienced tracking error can deviate significantly.

Stress testing: Mixed Results

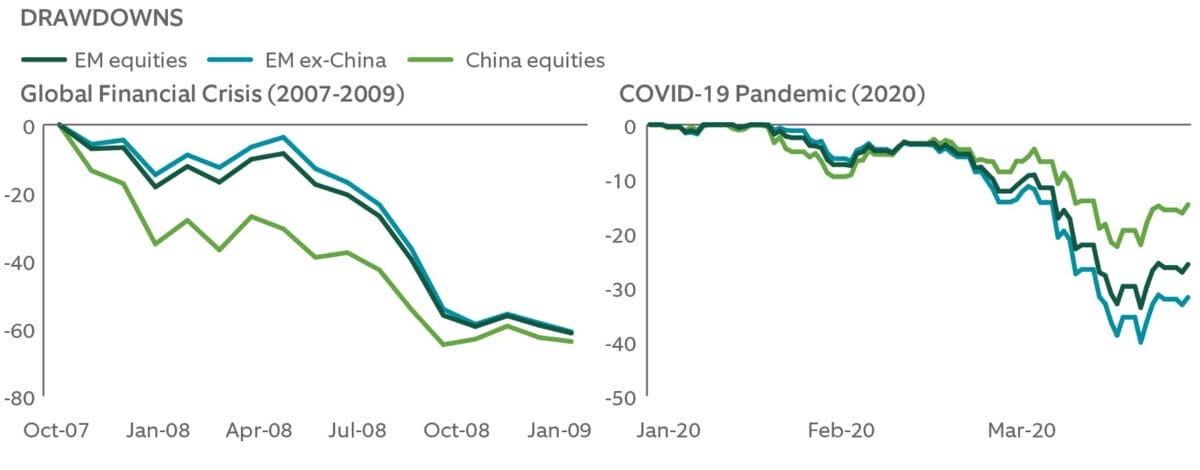

During times of market stress, even seemingly minor decisions can have an outsized effect. We examined the performance of Chinese equities and emerging markets equities, both with and without China, during the most recent downturns — the Global Financial Crisis and the COVID-19 pandemic. China modestly protected to the downside during the onset of the pandemic in the first quarter of 2020, but slightly exacerbated the drawdown during the Global Financial Crisis.

EXHIBIT 3

Source: Northern Trust Asset Management, Morningstar. Drawdown is the decline from a recent peak using monthly returns. Global Financial Crisis data is monthly from September 30, 2007 through February 28, 2009. COVID-19 period data is daily from December 31, 2019 to March 31, 2020, representing the onset of the pandemic. Historical trends are not predictive of future results. EM equities = MSCI Emerging Markets Index. EM ex-China = MSCI Emerging Markets ex-China Index. China equities = MSCI China Index. Historical trends are not predictive of future results.

Regional analysis: Asia-Pacific remains influential without China

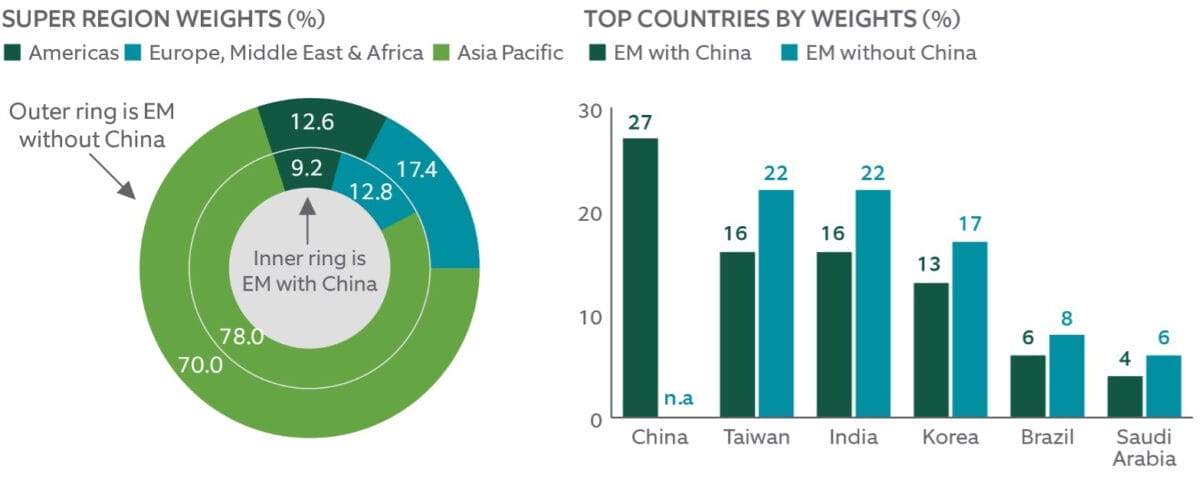

Next, we looked at China’s effect on index composition through regional and country weights. We note that removing Chinese companies doesn’t remove all Chinese revenues or input costs, thanks to non-Chinese multi-nationals throughout Asia.

The MSCI Emerging Markets Index contains a 78 per cent allocation to the Asia-Pacific region. Even when removing China and its 27 per cent weight, Asia-Pacific still represents 70 per cent of the remaining index due to the significant weights of other markets in the region, including 22 per cent for Taiwan, 22 per cent for India and 17 per cent for Korea. So even though investors can remove or manage direct exposure to China, Asia-Pacific’s presence remains strong with influence from the other key countries in the region.

EXHIBIT 4

Source: Northern Trust Asset Management, Bloomberg. Weights as of June 30, 2023 using IMI indices. It is not possible to invest directly in any index. Indexes are the property of their respective owners, all rights reserved.

China exposure: All or nothing?

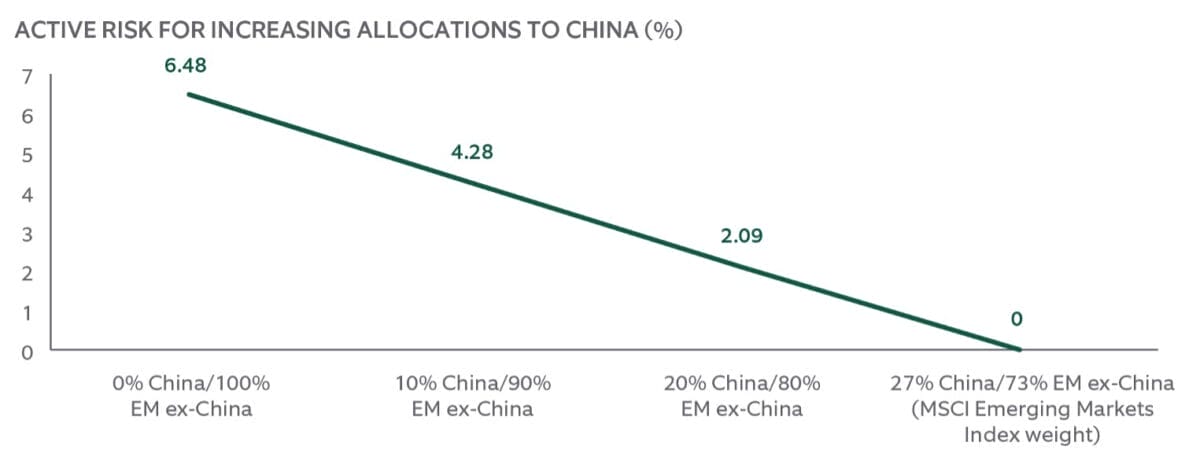

With the possibility that China’s weight in the MSCI Emerging Markets Index may grow even larger in the years to come, investors may want to maintain passive exposure but not at the weights dictated by the broader benchmark. To help control risk, investors can create custom weights by investing in MSCI China and MSCI ex-China separately.

We compared the expected active risk, versus the MSCI Emerging Markets Index, of portfolios comprising varying allocations to the MSCI China Index and MSCI Emerging Markets ex-China Index. Similar to tracking error, active risk represents the amount of risk investors take versus the MSCI Emerging Markets Index, with a higher percentage indicating more risk of underperforming the index. Active risk falls to zero for the portfolio with a 27 per cent weight to the China index and 73 per cent weight to the emerging markets ex-China index, because that portfolio represents the MSCI Emerging Markets Index, which had a weighting of 27 per cent to China as of June 30, 2023.

Fully excluding China results in an expected active risk of 6.48 per cent, which may not be palatable for benchmark-aware investors. A more modest approach of adjusting the weight of China to, say, 20 per cent would result in an expected active risk of 2.09 per cent, which may be more acceptable. Investors who take this custom approach to weighting China may wish to align the decision with their target benchmark. In other words, choosing to avoid investing in China but leaving one’s target benchmark as MSCI Emerging Markets may create misalignment in the risk budgeting process.

EXHIBIT 5

Source: Northern Trust Asset Management, Barra. Data as of June 30, 2023.Historical trends are not predicative of future results. China = MSCI China Index. EM ex-China = MSCI ex-China Emerging Markets Index.

Key Considerations for China in the Portfolio

Our analysis found that removing Chinese equities from a global index has enough of an impact on results that a thorough understanding is required. The tracking error of removing China from the portfolio is significant for emerging markets investors. Although the impact is less prevalent in a global context, for passive investors it is still not something that can be overlooked.

Rather than removing China altogether, another approach investors can take is to adjust their exposure to China through combinations of passive indexes.

Ultimately, this is a decision for each investor to make on their own, depending on their risk tolerance and views on the outlook for China. But we think investors, particularly passive index investors, do not necessarily need to accept China’s weight in the index as a given. There are options available for investors who wish to make adjustments.

Michael Hunstad is deputy chief investment officer and chief investment officer of global equities at Northern Trust Asset Management.

Leave a Comment

You must be logged in to post a comment.