Low fees have little correlation with fund performance or retirement outcomes, according to research conducted by SuperRatings.

This research stands in opposition to the Grattan Institute which called on the government to run a tender on default funds, as they claim there is little evidence that funds that charge higher fees provide better member services.

“The Grattan Institute has been a key driver of the unhealthy focus on fees, indicating that they have been too high across our industry – we don’t believe that is the case,” Adam Gee, SuperRatings chief executive, said. “There is opportunity on the admin side to reduce fees over time, but the Grattan Institute’s view that a default tender should be run purely on fees basis is not going to give significant savings to member outcomes.”

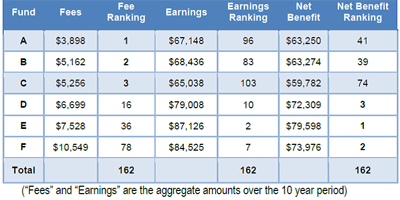

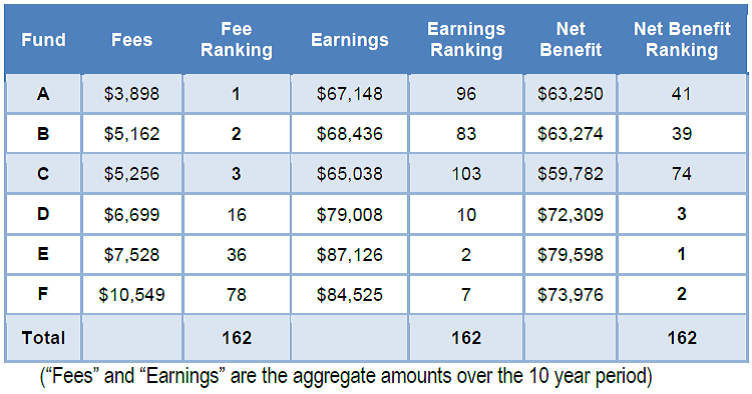

The SuperRatings review covered all major superannuation funds that have a 10 year performance history. The 162 funds had a net benefit calculation applied taking into account Superannuation Guarantee contributions, fees, taxes and investment returns over a 10 year period, based on an opening balance and salary of $50,000.

In the majority of cases, the funds with the lowest fees did not necessarily provide a better retirement outcome or return for its members. When asked if these results supported industry or retail funds Gee replied that it was balanced between the two with good and bad outcomes occurring in both.

He added fees are, at best, only loosely correlated with value and any assessment of a superannuation fund should be made using a broad range of criteria, with net benefit (investment returns less all implicit fees and taxes) being the only “meaningful basis for comparison of fees and investment performance”.

To demonstrate this point SuperRatings compared the three funds with the lowest fees and the three best performing funds based on net benefit (see table).

(source: SuperRatings)

In their analysis SuperRatings said the funds that charged the lowest fees generally showed underperformance in relation to their investment earnings. For example, Fund A, which charged the lowest fees during the ten year period, produced investment earnings ranked 96th out of the total 162 funds. The combination of Fund A’s low fees and investment earnings only ranked 41st on a net benefit basis.

However, the funds that produced the highest net benefit for their members did not have the cheapest fees. For example, Fund F which had the second highest net benefit was ranked 78th on the low fee scale, just below the industry median.

“Our analysis suggests there can clearly be an inverse relationship between fees and outcomes for members. This certainly supports our view that a tender process based purely on fees will not improve the retirement outcomes for most people,” Gee said.

Leave a Comment

You must be logged in to post a comment.