Australia’s largest asset owners will continue to insource investment management in the year ahead, as they explore ways to combine the benefits of active management with lower costs.

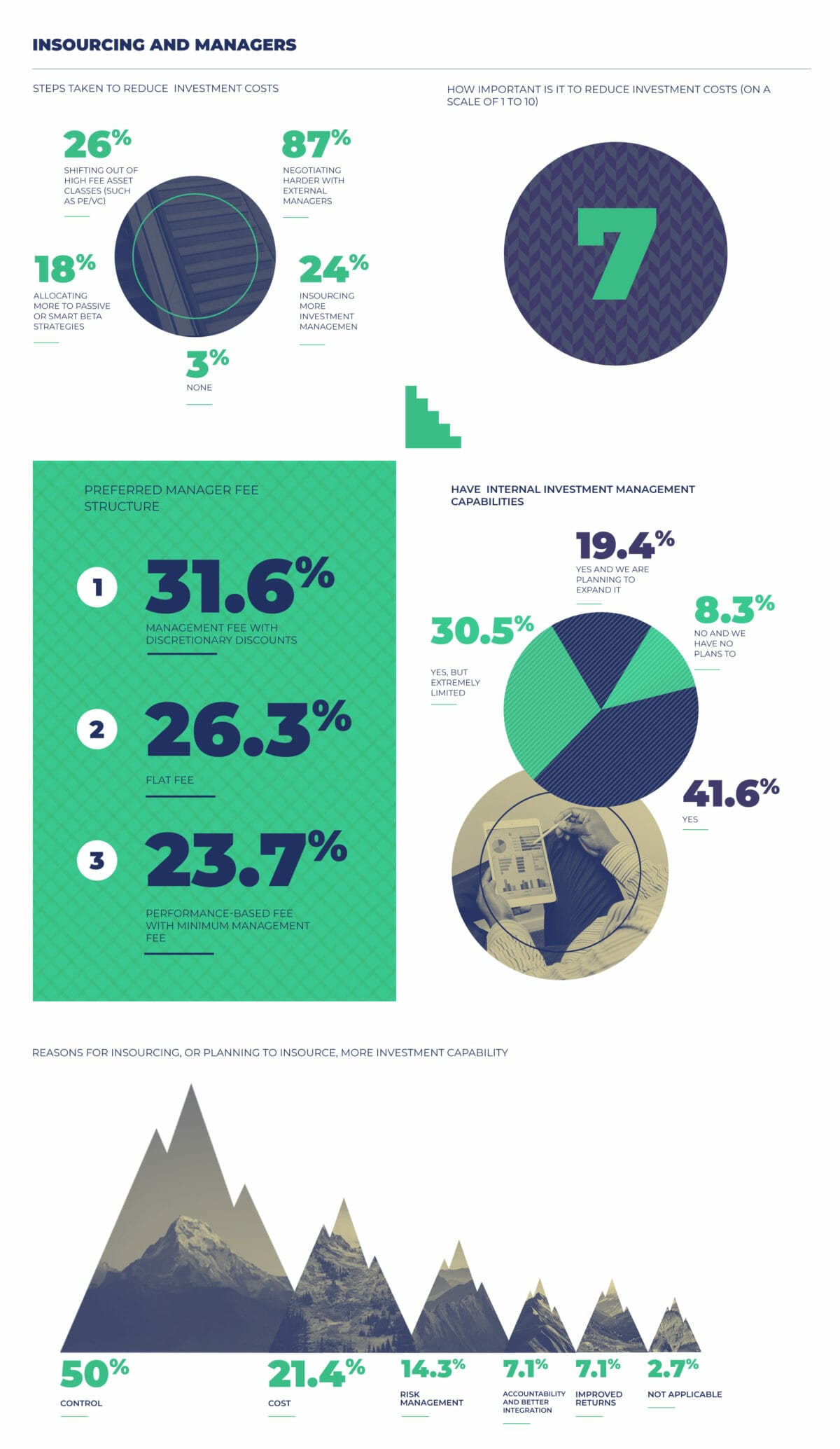

The 2017 Investment Magazine CIO Sentiment Survey found that 87 per cent of funds already have insourced funds management capability to some degree, although 29 per cent say they have only a limited capacity. Almost 20 per cent of CIOs said they have plans to expand an existing internal capability.

More than a third of CIOs who have insourced management say the main reason was to gain greater control over the investment process, and about 15 per cent said the main reason was to cut costs.

The investment chiefs of the 100 largest institutional asset owners in Australia, New Zealand and Papua New Guinea were invited to take part in the sixth-annual Investment Magazine CIO Sentiment Survey, conducted online over three weeks in October 2017.

The 38 respondents to the survey came primarily from local superannuation funds and control collective funds under management of almost $830 billion. While all respondents had their identity verified, their answers were anonymised. The 2017 survey was produced in association with Frontier Advisors.

Frontier director of investment strategy Chris Trevillyan said the trend towards insourcing reflects funds “shooting for the best of both worlds” – delivering excess returns at lower cost.

Trevillyan tipped that more funds would probably begin building internal investment teams once they reached a certain scale. As funds move into the $5 billion to $10 billion funds under management range, insourcing becomes a more viable proposition.

SuperRatings chief executive Kirby Rappell said funds would tread carefully in making the decision to insource.

“It’s not going to be a one-size-fits-all approach,” Rappell said.

He said best practice is for funds to assess each asset class individually, and to note where each class is in the investment cycle.

“Not everyone is coming to the same conclusion,” he said. “If we look at equities, for example, some funds are saying, ‘Yes, we believe there’s value to be had there.’ Other funds are saying they can access what they want from external managers very cost-competitively, and would rather not be exposed to that operational risk.”

He said that even though all funds were ultimately “solving for the same problem”, which is to maximise the outcome for fund members with the least amount of risk, “there’s a lot of divergence in the way they go about it”.

The survey found that CIOs plan to cut costs by moving out of high-fee asset classes, including venture capital and private equity, and by putting the squeeze on external managers.

Trevillyan said private equity and venture capital carried fees disproportionate to their significance in portfolios.

“You could have 5 per cent of your fund in, say, private equity, and it can constitute 40 to 50 per cent of the fee to the fund,” he explained. “When you’ve got those sorts of fee metrics, it does start to have an impact. It doesn’t mean people completely get out of private equity, but they reduce the allocation, and it’s certainly more targeted.”

A staggering 87 per cent of CIOs said they planned to negotiate harder with external managers on fees.

Trevillyan said CIOs are “entirely justified” in this. “Fund managers have been earning a lot of money for a long time,” he said. “They are extremely profitable businesses”.

Rappell said asset owners have had only limited success with such negotiations to date.

“As these funds grow, the marginal cost of funds management is not exactly the same as the increase in net assets, so funds will be looking to drive scale benefits,” he said. “It’s been a real challenge for a lot of the industry to drive scale benefits as much as they would like. I can’t see there being a reduction in funds’ focus on making sure they’re getting a good deal from their managers.”

On the actual structure of management fees, the survey found little agreement among CIOs. When asked to nominate their preferred structure, 32 per cent of respondents favoured a discretionary discount applied by the manager; 26 per cent preferred a flat fee; and 24 per cent wanted a minimum management fee plus performance fee.

“It does depend on the manager, the asset class, and just the beliefs of the investor,” Trevillyan said. “Some see performance fees as really aligning; others see it just means you can be paying very high fees. It shows it is a complicated area.”

Leave a Comment

You must be logged in to post a comment.