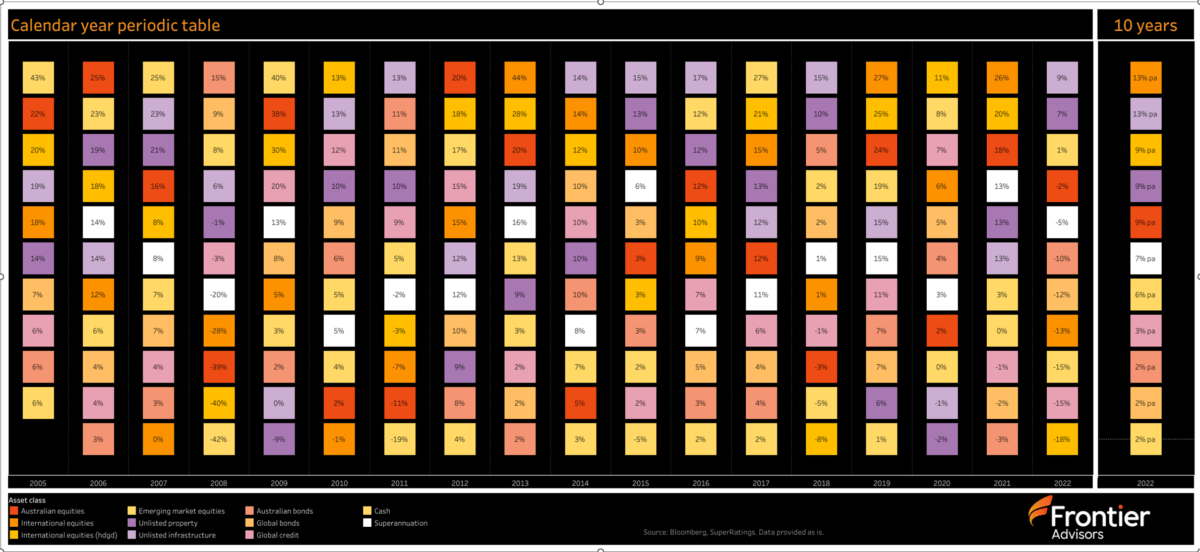

The 2022 calendar year suffered through a bear market in equities, the highest inflation surge since the 1970s, and the worst year on record for investment grade fixed income. US stocks fell sharply with the technology sector taking the heaviest hit.

The US Treasury yield curve was the most inverted since the early 1980s, highlighting the risk of recession in 2023. Over the year unlisted infrastructure (9 per cent), unlisted property (7 per cent) and cash (1 per cent) had positive returns, while every other asset class returned negative, ranging from Australian equities (-2 per cent) to international equities − hedged (-18 per cent).

Superannuation performance

Performance was quite weak for MySuper options. Most funds produced negative returns, with performance across the top ten funds ranging from -3.6 per cent to 1.7 per cent. Strategies with a larger proportion of unlisted assets across infrastructure, property and private equity performed better.

Performance was quite weak for MySuper options. Most funds produced negative returns, with performance across the top ten funds ranging from -3.6 per cent to 1.7 per cent. Strategies with a larger proportion of unlisted assets across infrastructure, property and private equity performed better.

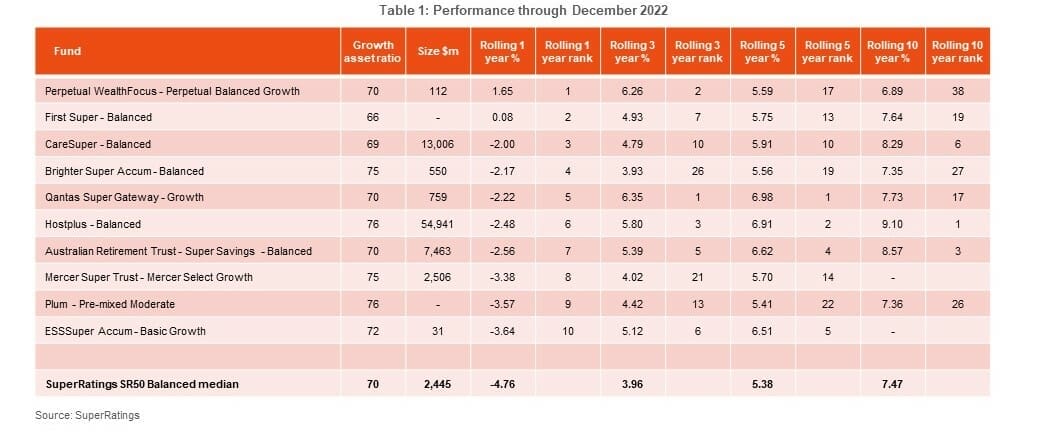

Table 1 ranks performance of the top ten super funds covered by the SuperRatings reporting, for the one-year period to 31 December 2022. It includes growth asset ratio, size of the fund, as well as multiple rolling time periods through ten years.

Table 1: Performance through December 2022

Risk and return

Risk and return

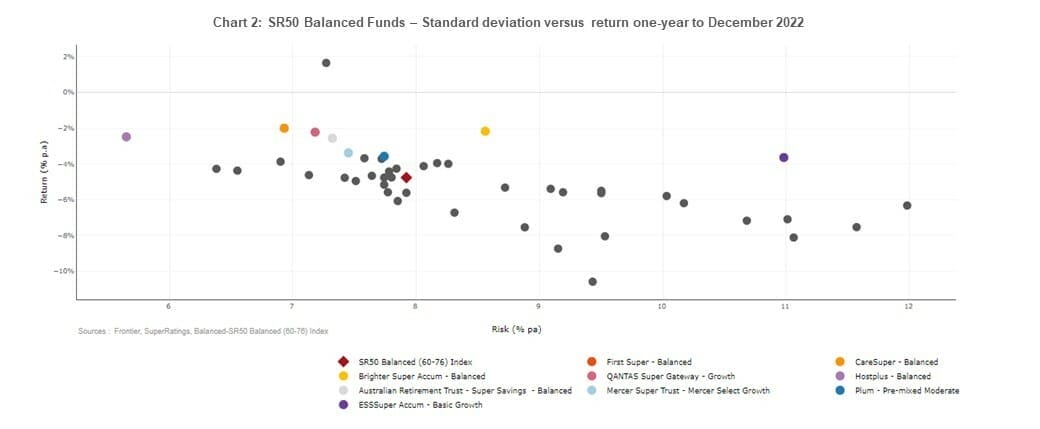

The majority of the top ten funds exhibited lower standard deviation than the median with the exception of Brighter Super and ESSSuper Basic Growth. Chart 2 shows performance and risk as defined by standard deviation of returns through one-year to December 2022.

Chart 2: SR50 Balanced Funds – Standard deviation versus return one-year to December 2022

Asset allocation

Asset allocation

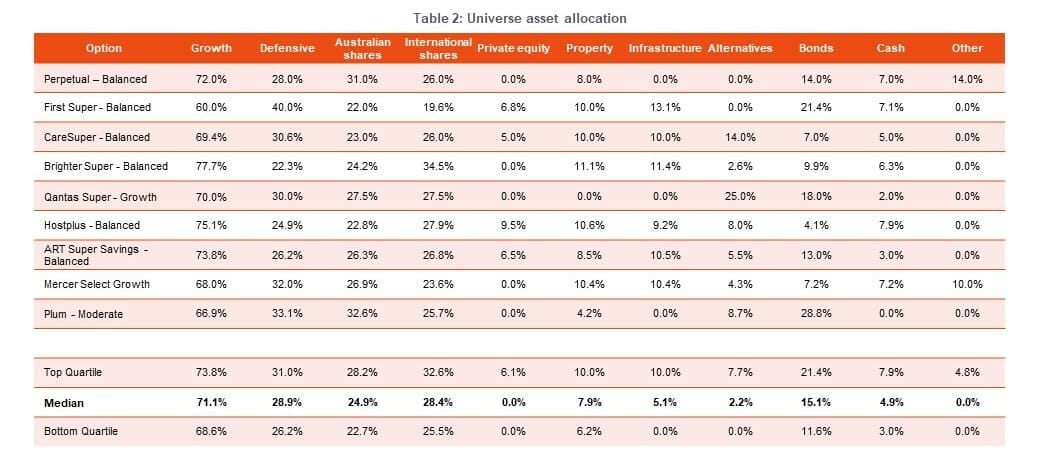

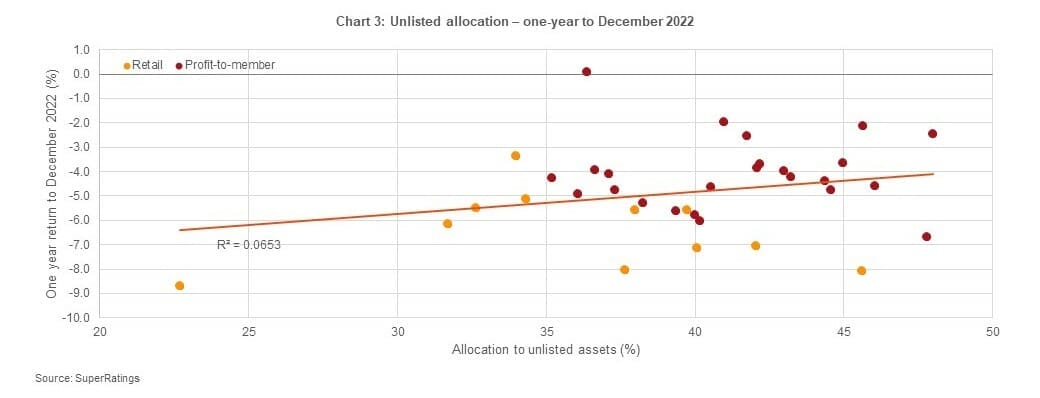

Based on the most recent asset allocations for the funds available, shown in table 2, funds with greater exposure to unlisted assets across private equity, property and infrastructure performed well (noting some funds classify these exposures as alternatives or other). Some of the top ten funds have not submitted timely allocation data.

Allocation to unlisted infrastructure, property and private equity were the most significant factors that contributed to absolute performance during 2022. While the coefficients of determination are not very high at 0.07, the line of best fit is upward sloping and shows a positive correlation with performance in diversified balanced portfolio throughout the year.

Allocation to unlisted infrastructure, property and private equity were the most significant factors that contributed to absolute performance during 2022. While the coefficients of determination are not very high at 0.07, the line of best fit is upward sloping and shows a positive correlation with performance in diversified balanced portfolio throughout the year.

These positive returns and correlations can be attributed to the managers’ and funds’ valuation processes, which involve the use of various methodologies. Although the valuation of unlisted assets are frequently criticised having shallower or no drawdowns in down markets, these assets are generally held longer term and often large, lumpy and illiquid and tend to be correlated with listed markets over the longer term despite short term differences.

Longer term performance

Longer term performance

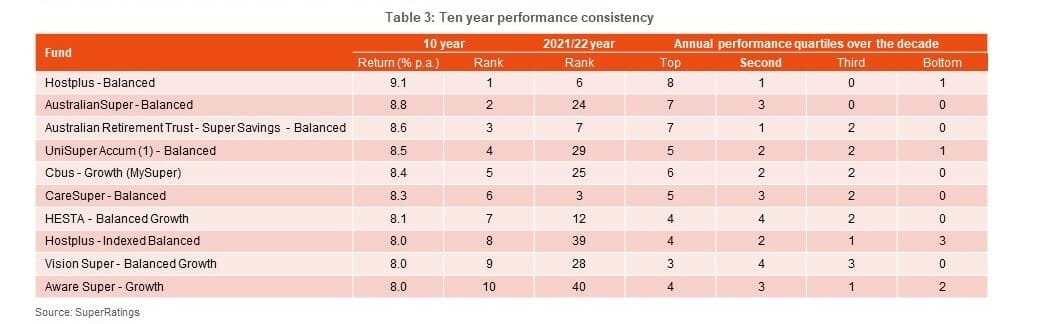

With superannuation a long-term investment, members should be looking for a fund with good performance consistency rather than just one good year. Table 3 examines the performance of the top ten funds over the ten years to December 2022. Only three of these funds were ranked in the top ten for the year just ended. Even more interestingly, four of the funds were below average over 2022.

AustralianSuper stands alone in terms of performance consistency in this analysis – it is the only fund which has outperformed the average fund in each of the last ten financial years. Somewhat unsurprisingly, given their higher allocation to growth assets and younger membership demographic, Hostplus has mostly appeared near the top or the bottom, in individual years – much more frequently in the former.

Most of these funds have had two or more years when their performance in a year has been below average. Only three funds have had at least one year when their return ranked them in the bottom quartile of peers.

The lesson from this analysis is that a single year of good performance does not necessarily result in good long-term performance. Similarly, a couple of underperforming years across a decade does not necessarily translate to poor longer-term returns.

Longer-term performance versus YFYS outcome

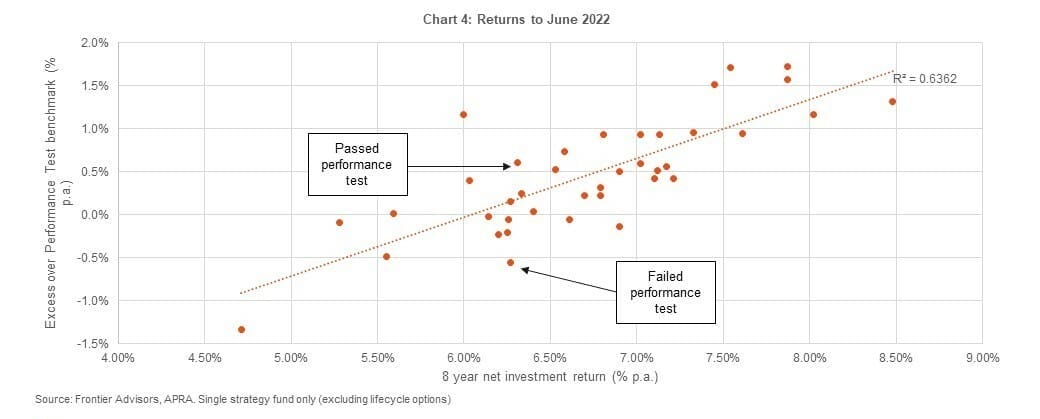

Funds which have better long-term performance typically had a higher performance test result. However, this relationship does not completely explain the outcomes – a number of funds had anomalous outcomes.

Chart 4 shows the actual performance of each MySuper option compared to its YFYS performance test outcome. In the chart we have highlighted two funds which both returned 6.3% p.a. over the 8 years – however, one fund outperformed their test by 0.6 per cent while the other fund underperformed by 0.6 per cent (and failed the test).

Warren Buffett, one of the most successful investors, would likely fail the APRA test due to underperformance compared to the S&P 500 index. Although this is against one asset class and is a hypothetical, this questions the value of a test that would declare such a successful investor a failure.

Analysing long term returns

Superannuation is a long-term investment, and it is long-term returns which impact member outcomes. Analysing short-term performance can be helpful, especially in understanding how performance was achieved and whether there are any trends. Waiting ten years to determine a fund is persistently underperforming will negatively affect a members’ final benefits.

However, basing an assessment of a fund on one year of good performance has limitations. As we have highlighted in this report, the level of risk and the underlying asset allocations will affect each fund’s ranking in any individual year. Basing an assessment on longer-term performance has more appeal. However, care is needed to differentiate between those funds which have done well in the past and those funds which may do well in the future.

A robust assessment across a wider range of factors is needed to satisfy each fund is of appropriate quality and provides good value for members. A ‘bright line’ test based on a single metric will misrepresent the complexity of ‘past performance being a guide to the future’. Instead, we believe a better outcome comes from analysing:

- Investment performance measured across multiple time periods and consideration of the level and nature of investment risk;

- Level of fees and costs, particularly where these are increasing;

- Size of assets and cashflow position, especially if the cashflow is negative;

- Fund governance, business management and trustee oversight; and

- Other factors such as member services and other qualitative factors.

David Carruthers is a principal consultant and Dan Leslie a senior consultant at Frontier Advisors.

Leave a Comment

You must be logged in to post a comment.