Unlisted assets can enhance super fund portfolios. Benefits include access to a broader opportunity set that affords better diversification and more return-seeking opportunities. Excellent governance is the entry ticket to these opportunities.

APRA’s recently released SPG 530 (Prudential Practice Guide – Investment Governance) addresses broader governance issues around use of unlisted assets by super funds. It pays considerable attention to valuation governance.

In effect, the regulator has moved this aspect of member equity from a secondary to a primary consideration. SPG 530 details that trustees require frameworks to ensure that beneficiaries transact at fair prices across all investment options.

Beyond the regulatory scrutiny, the glare of the media spotlight shines brightly on the industry on the valuation issue. This creates a situation where the behaviour of some funds can impact the overall perception of the industry.

While valuations are important, there is much more to the governance of unlisted assets. In this article, we explore some issues around good governance and management of illiquid assets, focusing on how they relate to fund flows. The relevance of flows is that they create a need to buy or sell, which is much harder to do with unlisted assets.

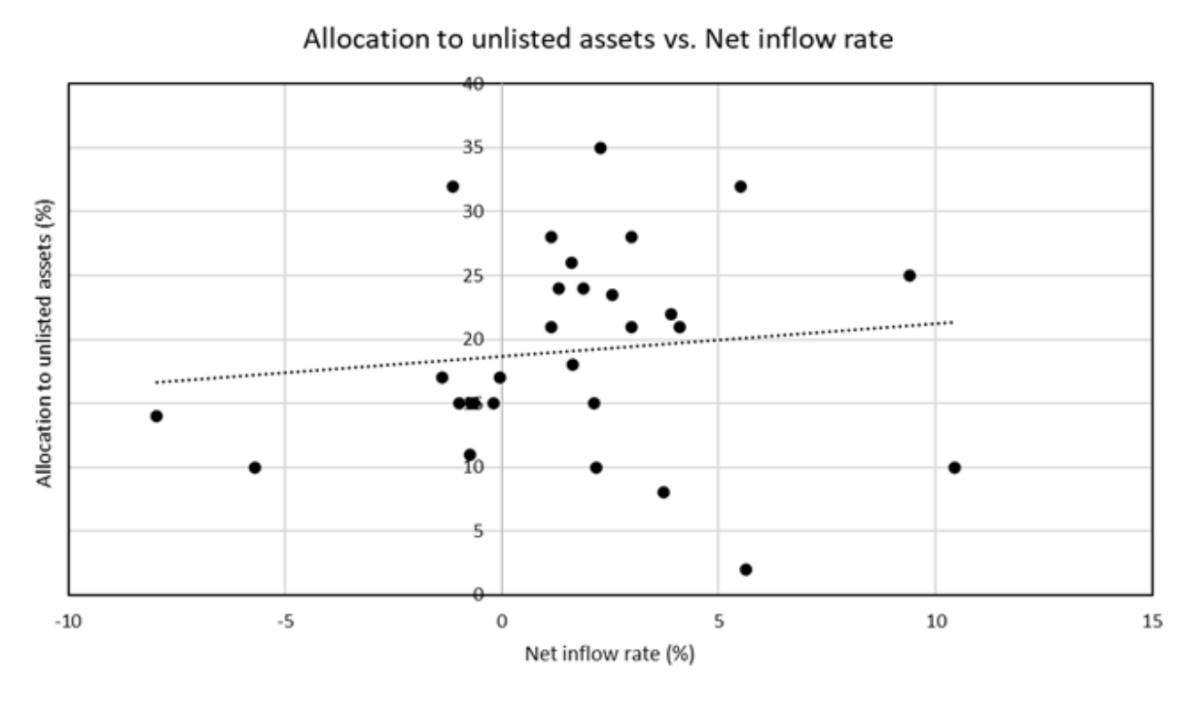

To set the scene, we were able to create the chart below using data from APRA alongside proprietary data provided by research house Chant West. It plots allocations to unlisted assets against the observed net inflow rates for a collection of MySuper options.

One might expect a strong positive relationship between net inflow rate and the allocation to unlisted assets. But the chart reveals only a modest positive relationship. Our fitted line slopes slightly up, and doesn’t fit the data particularly well.

Do we have a problem here? Do some funds have allocations to unlisted assets that are too high relative to their inflow profile, when compared against the behaviour of other funds?

Before jumping to conclusions, let’s first make some qualifications.

For starters, a fund doesn’t need to allocate a high proportion of its portfolio to unlisted assets simply because it has a positive net inflow profile. Further, there are significant differences between assets in the unlisted universe pertaining to liquidity, pricing, and risk, reducing the insights that can be drawn from aggregate analysis.

Also, funds may have different views on the attractiveness of unlisted assets relative to listed. In addition, there is the ability to identify and source opportunities in a competitive marketplace. (This is partly motivating development of offshore investment teams by some funds, to be closer to the dealmaking action). Further, a fund may have historically had a low allocation to unlisted assets, and it can take time to uplift the allocation.

More technical issues that impact on allocations to unlisted assets are not captured by examining simple inflow data.

For example, currency hedging can create large demands on liquidity in some situations. When the Australian dollar falls, forward currency hedges need to be paid out in cash, which can be problematic if assets are difficult to sell. Thus the structure of the overall allocation to global assets and the desired level of currency hedging come into play.

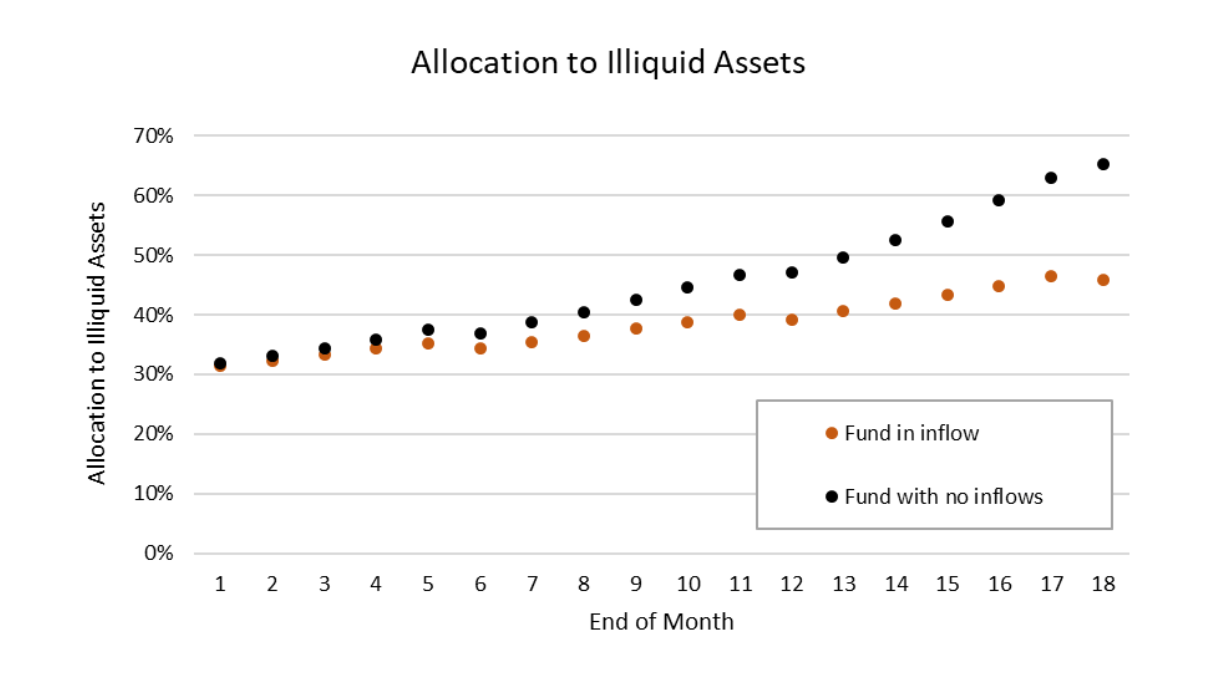

A related element of good governance of portfolios with unlisted assets – one that is not explicitly identified by APRA in SPG 530 – is the potential for a portfolio to “lose shape”. It is difficult to rebalance portfolios containing illiquid assets. This is a problem that only increases with the weighting to unlisted assets.

Positive net inflows can help to re-balance a portfolio back into shape. This is illustrated in the diagram below comparing two funds with different inflow profiles during a market scenario that approximates the Global Financial Crisis.

Is there a risk that some funds are taking inadvertent liquidity bets through their unlisted asset exposures? Across the universe of funds, a few funds do seem to have an outsized exposure to unlisted assets relative to peer funds in similar situations. Hopefully these funds have the strongest governance practices, and have done all the analysis and risk assessment to support their position.

Where all this leads is that good governance for portfolios with illiquid assets extend beyond just valuation governance. Governance of unlisted asset investment programs, including the implications for portfolio structure and liquidity management, sits as an overarching issue.

Which leads us to a recommendation. As part of their governance practices around the use of illiquid assets, super funds should be undertaking scenario analysis to assess the potential for liquidity stress and loss of portfolio shape arising from inability to readily trade. The aim would be to ensure that the strategic asset allocation to unlisted assets is well informed and does not exceed prudent bounds.

David Bell is executive director and Geoff Warren is research director of The Conexus Institute, an independent think-tank funded philanthropically by Conexus Financial, publisher of Investment Magazine.

Leave a Comment

You must be logged in to post a comment.