Elon Musk seeks to make life “multiplanetary” by colonising Mars, and this is an expensive endeavour. Musk believes he has a moral obligation to direct his wealth toward that goal and viewed his US$55.8 billion ($85 billion) performance package at Tesla as a means of bankrolling that mission.

This was the colourful case background summary of Delaware Court of Chancery judge Kathaleen St. Jude McCormick, who in late January rescinded Musk’s 2018 package because Tesla was unable to prove that the package was entirely fair.

In her post-trial opinion McCormick took plenty of pot shots at Musk and also gave a harsh appraisal other Tesla directors, including its Australian chair Robyn Denholm.

McCormick’s ruling raised not only a range of significant corporate governance issues – especially when it comes to the influence “Superstar CEOs” wield over board members – but also the role of the courts in deciding whether a remuneration package is fair.

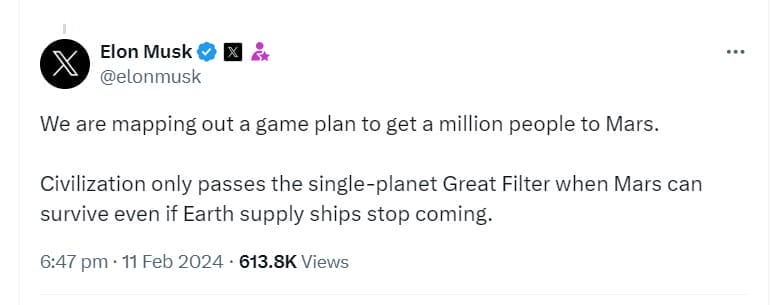

Musk, meanwhile, says he plans to move Tesla’s incorporation to Texas in protest and is pushing ahead with plans get a million people on Mars (having already moved SpaceX to Texas).

Superstar CEOs

McCormick’s colourful opinion drew upon a recently published European Corporate Governance Institute (ECGI) working paper Superstar CEOs and Corporate Law written by Assaf Hamdani and Kobi Kastiel.

Superstar CEOs are individuals whom directors, investors and markets believe make a unique contribution to company value.

“Markets may believe, for example, that only the CEO possesses the idiosyncratic vision that is essential to make the company outperform the competition. Or that only she possesses exceptional skills or other rare qualities that are crucial for implementing the company’s strategy,” the authors say.

“The source of their power is not the misalignment of interests between directors and shareholders, shareholder passivity, or the formal power that CEOs exercise in director elections. It is the market’s belief that the CEO has such a unique vision or leadership skills that the company’s success depends on that CEO’s continued leadership.”

The working paper notes that for many years, corporate governance reforms focused on empowering shareholders, making directors more independent, and bolstering their accountability to shareholders. The aim of these reforms was ensuring that boards would be well positioned to monitor CEOs and to make sure that their interests align with those of shareholders.

But the power of Superstar CEOs can be difficult for boards and shareholders to contain. “Boards may have only limited ability to exercise oversight over CEOs who are perceived as uniquely valuable. Superstar CEOs can undermine directors’ effectiveness in reviewing corporate strategy, approving major transactions, or even preventing CEOs from engaging in improper behaviour”.

As long as the CEO is perceived as a star and the company depends on their vision and leadership, “even nominally independent directors—those who have no business or other ties to the CEOs and who are genuinely committed to shareholders—are less likely to challenge the CEO and may tolerate problematic practices that would normally be met with their resistance”.

Unduly deferential

In her opinion McCormick said CEO superstardom means even independent actors are likely to be “unduly deferential”.

“They doubt their own judgment and hesitate to question the decisions of their superstar CEO. They view CEO self-dealing as the trade-off for the CEO’s value. In essence, Superstar CEO status creates a ‘distortion field’ that interferes with board oversight.

“In the face of a Superstar CEO, it is even more imperative than usual for a company to employ robust protections for minority stockholders, such as staunchly independent directors. In this case, Tesla’s fiduciaries were not staunchly independent—quite the opposite,” McCormick said.

Overpaid?

McCormick began her post-trial opinion by asking “was the richest person in the world overpaid?”. But two hundred pages later, the question is not really answered (although McCormick believes she has).

Because McCormick decided Tesla’s proxy statement to shareholders “inaccurately described key directors as independent and misleadingly omitted details about the process”, the burden of proof shifted from the plaintiff Richard Tornetta (a former heavy metal drummer who held just nine shares) to Tesla and its directors.

So this meant McCormick had given the defendants what she described as the “unenviable task of proving the fairness of the largest potential compensation plan in the history of public markets”.

“Perhaps starry eyed by Musk’s superstar appeal, the board never asked the US$55.8 billion question: Was the plan even necessary for Tesla to retain Musk and achieve its goals?,” McCormick said.

Musk owned 21.9 per cent of Tesla when the board approved his compensation plan and McCormick said this gave him “every incentive to push Tesla to levels of transformative growth,” noting Musk stood to gain more than US$10 billion for every US$50 billion in market capitalization increase.

McCormick believes Musk had no intention of leaving Tesla, “and he made that clear at the outset of the process and throughout this litigation”. McCormick questioned why “the compensation plan was not conditioned on Musk devoting any set amount of time to Tesla because the board never proposed such a term”.

According to Musk, the time issue “was not raised in this compensation structure” because the idea was “silly.” Tesla director Todd Maron testified that the board did not ask for such a requirement because that “would have been like saying goodbye to Elon”.

The performance package granted stock option awards for approximately 304 million shares that Musk can buy at about US$23.33 each compared with Tesla’s current share price of about US$200. When/if Musk exercised any of the options he would have been required to hold the shares for five years before selling.

Some have been critical of McCormick, suggesting her ruling was judicial overreach and based on her personal view of what is “fair” based on personal view on the size of Musk’s compensation – which described as “unfathomable” rather than on the law.

Musk’s package, however, had been overwhelmingly approved by shareholders back in March 2018 and Musk had met all the package’s performance hurdles, dramatically increasing Tesla’s market capitalisation and providing windfall gains to shareholders.

While, the court may have ruled Tesla did not follow proper process in seeking shareholder approval, it is very likely most shareholders will be very happy with how things have panned out.

Voting power

Musk currently owns around 13 per cent of Tesla stock after selling large quantities of shares in 2022 to help finance his US$44 billion Twitter purchase. His voided options would have given him an effective stake of 20.5 per cent.

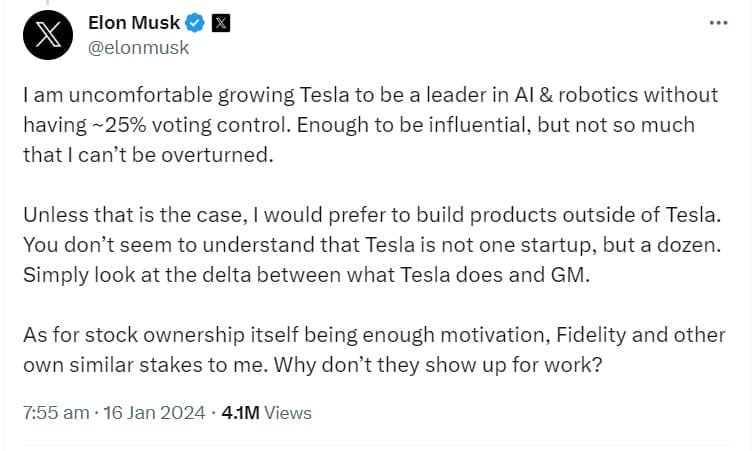

A couple of weeks before McCormick’s ruling Musk had also been pressuring the Tesla board to give him around 25 per cent voting control of the company, believing that was about “the right amount of voting influence” for him at Tesla.

Musk explained that “if I have 25 per cent, it means I am influential, but can be overridden if twice as many shareholders vote against me versus for me. At 15 per cent or lower, the for/against ratio to override me makes a takeover by dubious interests too easy.

“I would be fine with a dual class voting structure to achieve this, but am told it is impossible to achieve post-IPO in Delaware,” he said.

The Tesla board will come under extremely close scrutiny if and when Musk seeks to negotiate an arrangement that would give this voting power. The board also needs to decide whether it will be appealing McCormick’s decision and/or negotiating a new incentive package for Musk.

McCormick’s opinion focussed a good deal on the board’s lack of negotiation. Musk presented the board with an original proposal. He later revised his proposal. When he discovered his revision was too generous to himself, he revised it again.

Musk said his final proposal “was, I guess, me negotiating against myself”.

Leave a Comment

You must be logged in to post a comment.