The recent reforms to Australia’s foreign investment policy mirror what is happening in other jurisdictions around the world.

Heightened geopolitical tensions mean when it comes to foreign direct investment (FDI), the talk is now all about “friend-shoring”, “near-shoring”and investing in “geopolitically close countries”.

Treasury says “national security threats are increasing due to intensifying geopolitical competition, and in some cases, risks to Australia’s national interests from foreign investment have evolved”. This is why Australia is “strengthening its risk-based approach to assessing investment proposals”.

For an example, look no further than the Treasurer’s decision earlier this month forcing five China-linked investors to sell a 10 per cent shareholding in rare earth developer Northern Minerals (and to the cyberattack on the company that promptly followed).

FDI fracturing

A new UNCTAD report Global economic fracturing and shifting investment patterns says geopolitical differences are causing a “fracturing trend in global FDI”.

There has been a reduction in investments between “geopolitically distant” countries that reflects the “significant influence” geopolitical issues is now having on “investors’ location choices, overshadowing traditional determinants of FDI”, the report said.

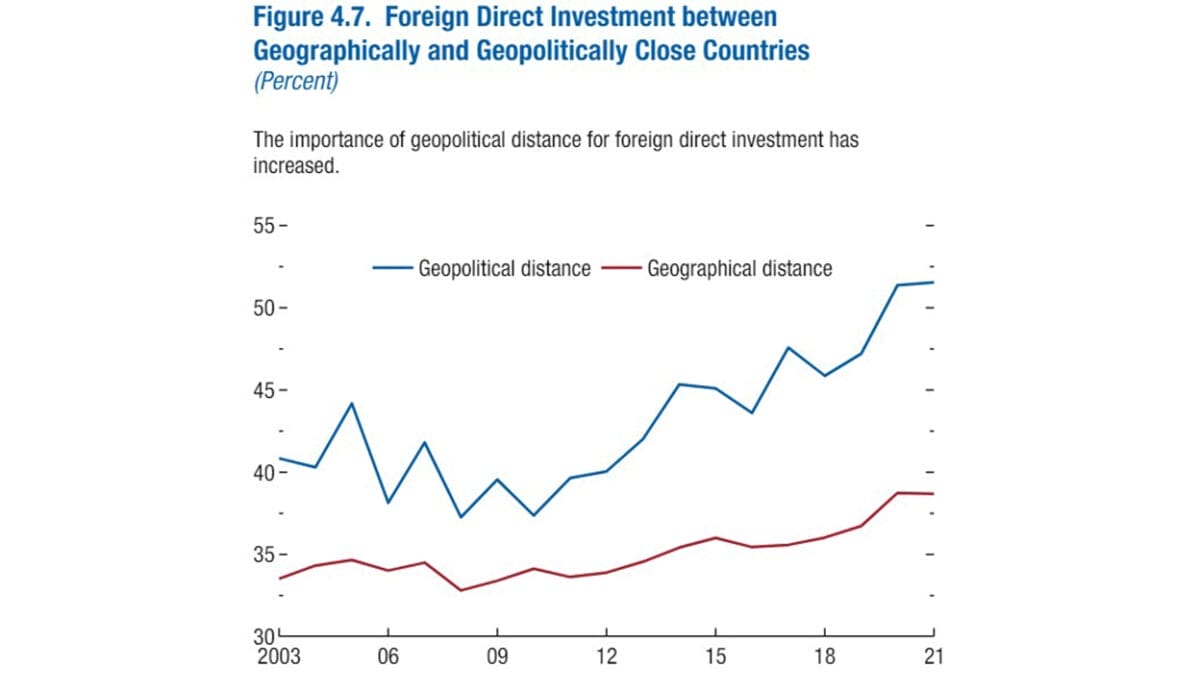

The International Monetary Fund (IMF) agrees rising geopolitical tensions are a key driver of FDI fragmentation, as bilateral FDI is increasingly concentrated among countries that share similar geopolitical views (see chart below).

IMF modelling suggests that that if this fragmentation continues, it “could substantially reduce global output, by about 2 per cent in the long term”.

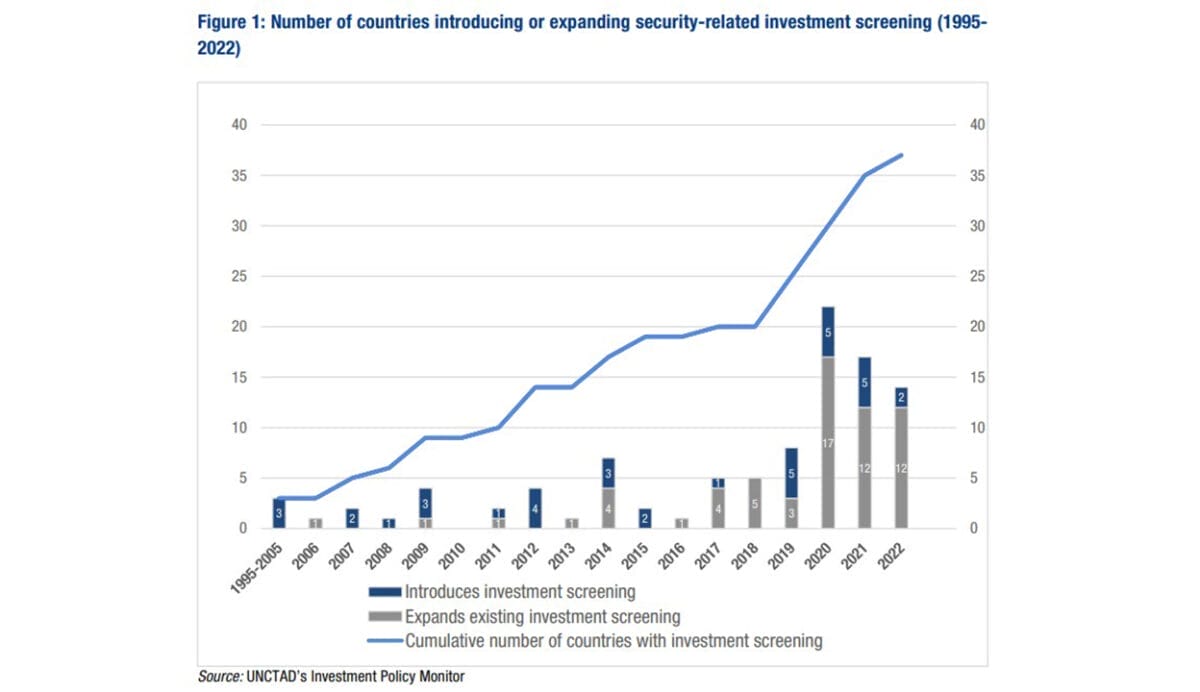

An earlier UNCTAD report The Evolution Of FDI Screening Mechanisms says FDI regulatory changes around the world in recent years have been chiefly focussed on expanding the scope of sectors targeted by Investment Screening Mechanisms (ISMs); covering new activities increasingly considered strategic; lowering the threshold rule triggering FDI review; and broadening the definition of investment or control that triggers screening.

The chart below shows the expansion of FDI screening.

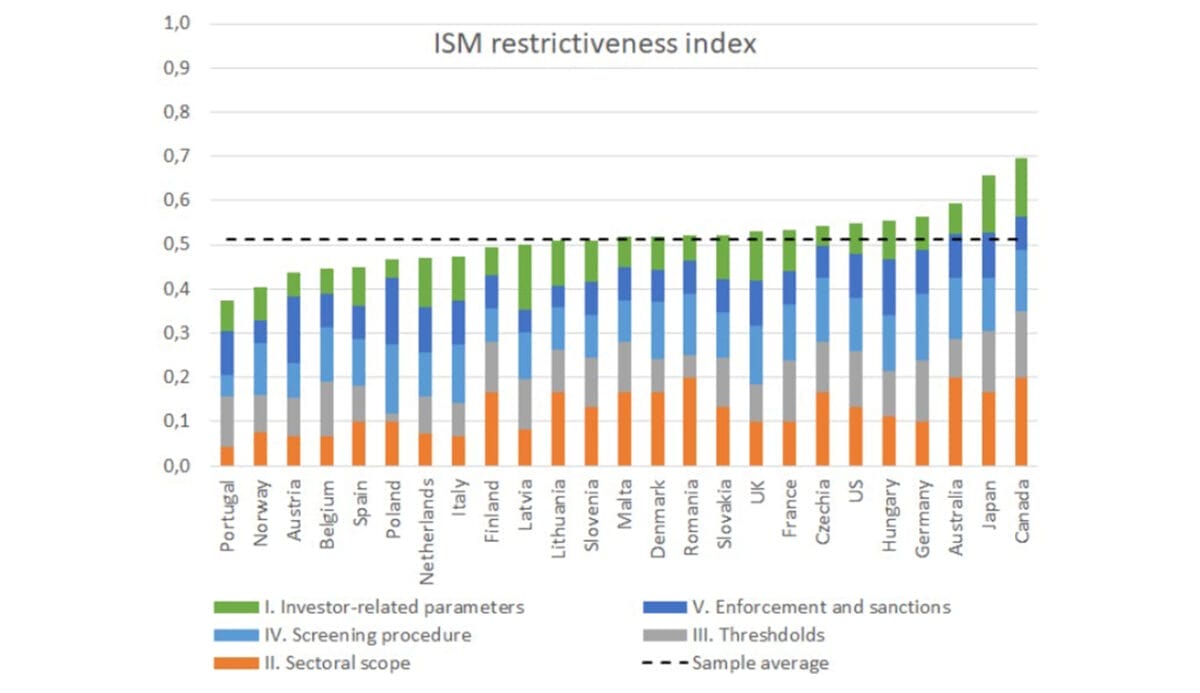

Interestingly, a Banque de France Working Paper Who’s Afraid of Foreign Investment Screening? (Bencivelli et al 2023), indicates Australia, Canada and Japan have the most “robust” ISMs.

Given the new stricter Foreign Investment Review Board (FIRB) regime Australia might now lead the paper’s ISM Restrictiveness Index (see graph below).

The paper notes that despite its ranking, Australia is still viewed as an attractive FI location.

Low-risk investors

Treasury says the new FIRB regime “will focus scrutiny on high-risk investments to protect our national interest, while streamlining low-risk investments to bring in the capital Australia needs quickly”.

It seems pretty clear that Chinese investment in Australia’s critical minerals will fall into the ‘high-risk’ category ’. But where will the ‘low-risk’ investment be coming from? The immediate/default example that is usually offered is Canadian pension funds.

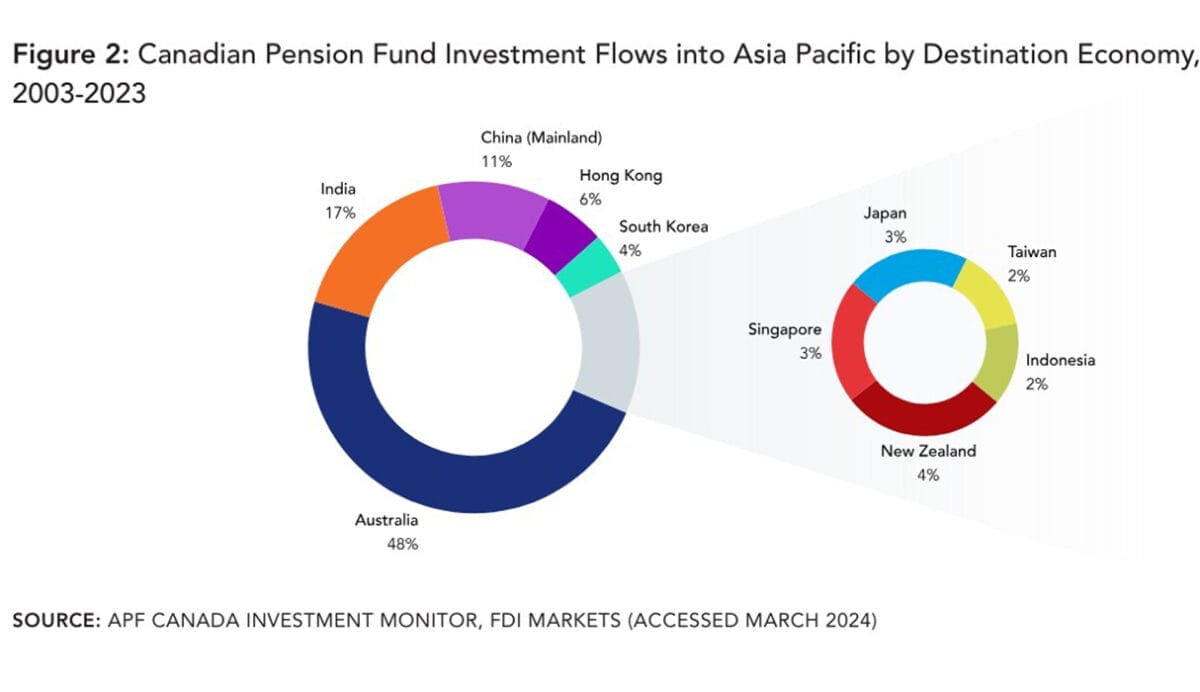

Australia has been the Asia Pacific region’s top recipient of Canadian pension fund investment flows (see chart below). From 2003 to 2018, Australia accounted for 45 per cent of these investment flows, with this increasing to over 50 per cent in 2019-23. Roughly C$30 billion ($33 billion) has been invested since 2018.

In recent years, Canada’s ‘Maple 8’ pension funds such Canada Pension Plan Investment Board (CPP Investments), Alberta Investment Management Corp (AIMco), Caisse de dépôt et placement du Québec (CDPQ), Ontario Teachers’ Pension Plan (Ontario Teachers;) Ontario Municipal Employees Retirement System (OMERS) and the Public Sector Pension Investment Board (PSP Investments), have made big investments in Australia in sectors such as agriculture, energy infrastructure and telecommunications.

In recent years, Canada’s ‘Maple 8’ pension funds such Canada Pension Plan Investment Board (CPP Investments), Alberta Investment Management Corp (AIMco), Caisse de dépôt et placement du Québec (CDPQ), Ontario Teachers’ Pension Plan (Ontario Teachers;) Ontario Municipal Employees Retirement System (OMERS) and the Public Sector Pension Investment Board (PSP Investments), have made big investments in Australia in sectors such as agriculture, energy infrastructure and telecommunications.

The Joint Statement by Canada and Australia on Cooperation on Critical Minerals released in March also says “ Canada and Australia share a like-minded approach to the development of global critical minerals supply chains, an approach driven by our strong environmental, social and governance (ESG) policies”.

Can we rely on Canadian pension funds?

There are, however, some question marks over whether Canadian money will continue flowing freely into Australia.

Canada’s pension funds are currently under pressure from the Canadian government, industry groups and others to stop investing so much of their assets under management (AUM) offshore.

In Canada’s recent 2024 Budget Government announced it was setting up a working group led by former Governor of the Bank of Canada, Stephen Polo, “to explore how to catalyze greater domestic investment opportunities for Canadian pension funds”.

The government says the working group will “identify priority investment opportunities that will grow Canadians’ pension savings – that meet Canadian pension plans’ fiduciary and actuarial responsibility, spur innovation, and drive economic growth”.

Applying even greater pressure, more than 90 Canadian business leaders recently signed an open letter to Finance Minister Chrystia Freeland and her provincial counterparts, urging them “to amend the rules governing pension funds to encourage them to invest in Canada”.

The letter claims Canadian pension funds have reduced their holdings of publicly traded Canadian companies from 28 per cent of total assets at the end of 2000 to less than 4 per cent at the end of 2023.

It claims the Maple 8 funds have more invested in China than they have in Canadian public and private equities and that their holdings of all Canadian-based equity investments, including public and private companies, real estate, and infrastructure, is down to approximately 10 per cent of total assets.

The group behind the letter is investment management group, Letko Brosseau. Stirring the pot, Letko Brosseau argues “Canada must start investing in itself” – Canada’s 3 per cent weight in the MSCI (World) Index is often referred to as an appropriate investment target.

“Using this bogey means that the smaller a country is, the less it should invest in itself, a patently inappropriate conclusion”.

The group has been circulating a document, Canadian Pension System’s Divestment of Canadian Assets: The Canary in the Coal Mine, that it claims explains the problem.

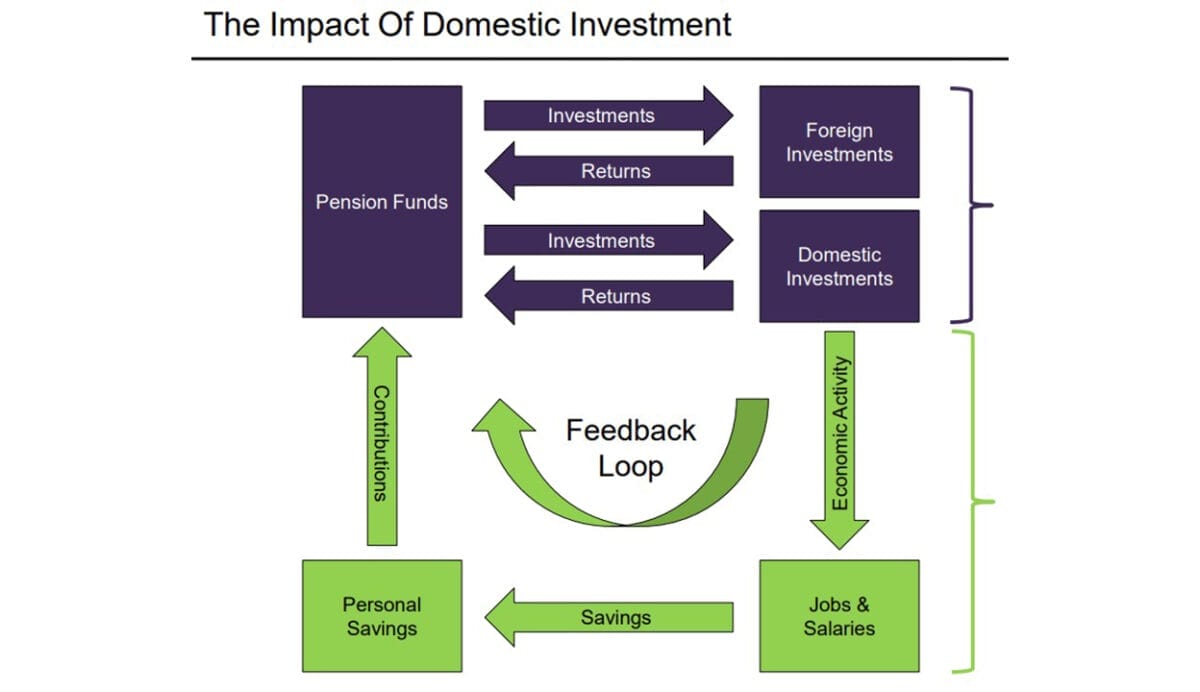

“The BLUE represents the world as viewed by pension investment managers. They see a world of investment opportunities, each presenting a certain risk and offering a return potential. Whether the investment is foreign or domestic makes little difference from their perspective.

“The GREEN represents the domestic economic system illustrating that domestic investments create domestic jobs which pay salaries, generate savings, and allow contributions into the pension funds. The GREEN cycle is not part of pension managers’ perspective,” Letko Brosseau (perhaps dubiously) claims.

Pension defence

OMERS invests and administers about C$130 billion. The pension fund says it is “dedicated to growing and fiercely defending” its members’ retirement savings. “We must put members’ interests first and foremost; above those of any self-interested parties with competing agendas,” OMERS says.

“We can do this while being a huge champion for Canada. Roughly 25 per cent our portfolio (C$34 billion) is invested here at home, notwithstanding the fact that Canada represents less than 3 per cent of global GDP”.

CPP Investments says it has increasingly become “a part of the public discourse on the best way to bolster the financial security of future generations. This includes whether public pension plans are investing enough in Canada”.

In its recently released 2024 Annual Report, CPP Investments claims (perhaps unconvincingly) that “the case is also clear for investing in Canada, which is why 12 per cent of our portfolio is invested here.

“ To put that into perspective, Canada makes up just 3 per cent of global GDP. We invest four times more than Canada’s global economic weight because we recognize the excellent investment opportunities in our home market”.

Trying to ward off the attacks, CPP Investments president and CEO John Graham notes that its governing CPPIB has no investment directions related to economic development, social objectives or political directives.

“Our independence from government is enshrined in carefully written legislation, ensuring that we can, and do, operate at arm’s length, free from political interference”.

By way of comparison, on 30 June 2023, 50.4 per cent of AustralianSuper’s (then) $299 billion in AUM was invested in Australia (which, by the way, has a smaller GDP than Canada).

Our biggest asset owner has indicated seven out of 10 new dollars is now being invested overseas, and extrapolations suggest that in four to five years’ time, AUM in Australia might have dropped to near 40 per cent.

So while Australia’s super funds may seem more patriotic than their Canadian counterparts, they may still be a little nervous when they are invited to the next Treasurer’s Investor Roundtable.

This will especially be the case if they continue the discussions from the last roundtable that Treasurer Jim Chalmers said was all about getting “capital flowing to where it’s needed most in our economy” and “investing in our national priorities”.

Leave a Comment

You must be logged in to post a comment.