Visiting the Valencia region a few days after the recent deadly floods, Spain’s King Felipe VI, Queen Letizia and Prime Minister Pedro Sánchez were heckled and pelted with mud by angry residents.

Sánchez had just ordered the largest peacetime military deployment in the nation’s history to help with search and clean-up efforts, and approved a €10.6 billion ($17.2 billion) relief package. After more massive street protests the Prime Minister later added another €3.8 billion to the package.

The floods were caused by a natural weather phenomenon known as DANA (Depresión Aislada en Niveles Altos). However, scientific experts say climate change’s impact on weather systems such as DANA contributed to its record-breaking rainfall.

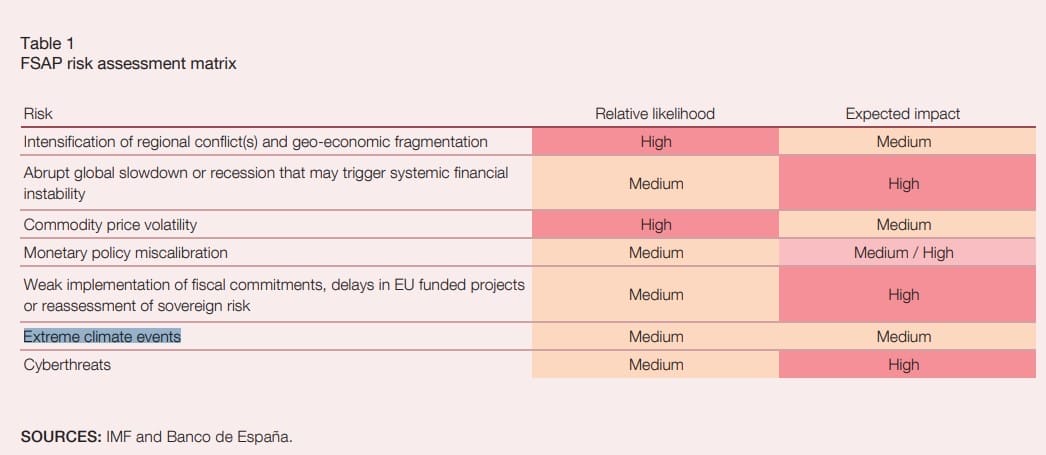

Presenting Banco de España’s latest Financial Stability Report (FSR) shortly after the floods, the central bank’s head of stability, Ángel Estrada, said the disaster showed climate risks were materialising faster than expected. Estrada said banks needed to focus more on assessing physical risks, not just transition risks.

Unfortunately, the Autumn FSR had devoted little space to climate issues, with Table 1 below showing Banco de España thought there were greater risks to worry about.

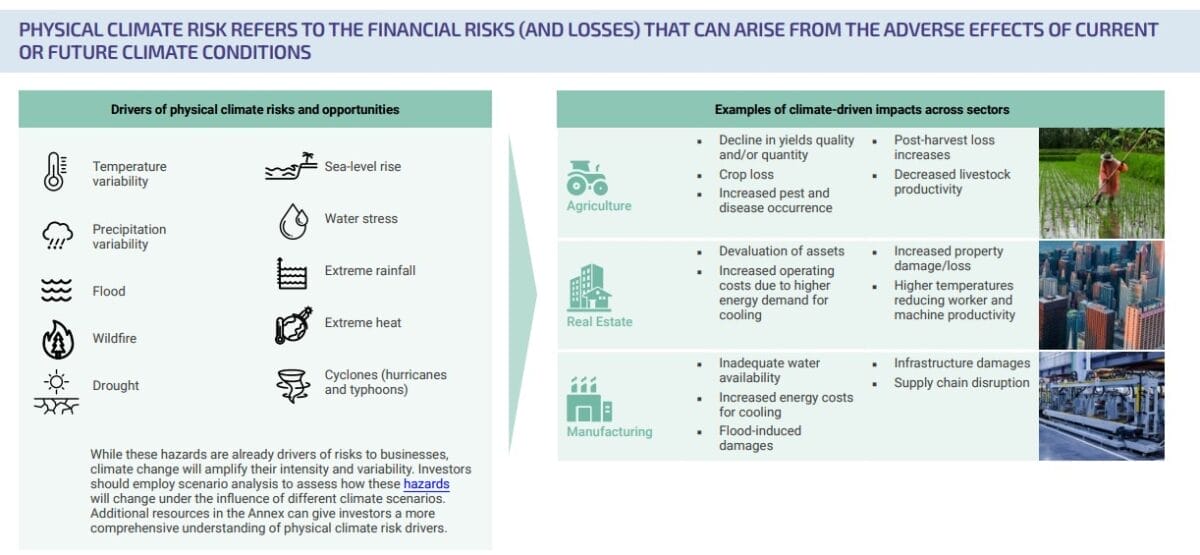

The UN Environment Program’s (UNEP) new Physical Climate Risk Assessment and Management: An investor playbook highlights the financial risks and losses that can arise from the adverse effects of current or future climate conditions.

The Playbook notes that while the climate hazards in the diagram below are already drivers of risks to businesses, climate change can amplify their intensity and variability.

Physical risks are typically split into two categories – long-term ‘chronic’ impacts resulting from increased temperatures, rising sea levels etc, and ‘acute’ impacts from extreme weather events (such as floods).

Investor belief

In a recent paper, How Does Climate Risk Affect Global Equity Valuations? A Novel Approach, the EDHEC-Risk Climate Impact Institute notes that up until now, transition risk has received more attention than physical risk when assessing how climate risk can affect asset valuations.

Investors often assume that the regulatory climate risks to a business are likely to be front-loaded and, therefore, more relevant to valuation than the more ‘distant’ physical damages that are expected to fade in significance by virtue of being ‘discounted away’.

However, the paper says “physical and transition costs are two sides of the same valuation coin: the greater the transition effort, the smaller the expected physical damages, and vice versa”.

The Institute argues current equity valuations seem to reflect investor belief that either strong and effective abatement action will be undertaken and climate change brought under control; or that climate change, even if poorly abated, will have a negligible effect on economic output and consumption.

“Since neither assumption should be considered a very likely scenario, we have argued that there is ample potential for equity revaluation,” it says.

This downward revaluation could range from a few percentage points to as much as 50 per cent, depending on factors such as the strength (or otherwise) of abatement policies and the nearness of tipping points.

The London Stock Exchange Group’s (LSEG) new COP 29 Net Zero Atlas agrees that investor thinking on climate risk has been dominated by a focus on transition risk “but as temperature records continue to tumble and extreme weather events become more frequent and debilitating, the physical risk climate change poses to societies and portfolios is beginning to receive attention”.

“These impacts are asserting themselves faster than expected, with recent forecasts suggesting annual damages attributed to climate change are likely to reach US$38 trillion ($58.1 trillion) by the mid-century under a 2°C warming scenario”.

Damage function

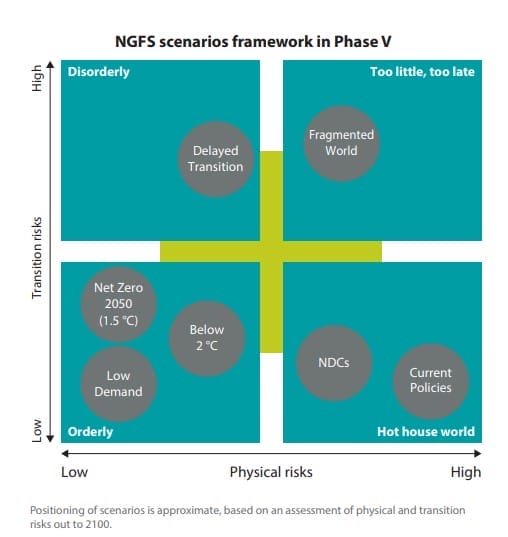

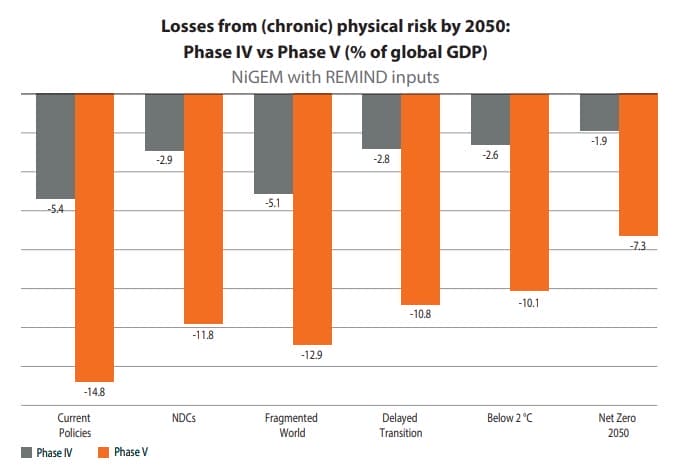

The Network for Greening the Financial System (NGFS) has also released a new version (Phase V) of its ‘scenarios’ (below) that applies a more comprehensive ‘damage function’ (which projects GDP losses based on increasing warming levels) to enhance its physical risk modelling.

Using the new damage function, the NGFS Current Policies scenario foresees GDP losses of around 15 per cent from chronic physical risk compared to a scenario without climate change by 2050.

Using the new damage function, the NGFS Current Policies scenario foresees GDP losses of around 15 per cent from chronic physical risk compared to a scenario without climate change by 2050.

Under NGFS’ previous Phase IV, losses from chronic physical risk were estimated at 5.4 per cent (see chart below).

Under the NGFS ‘Current Policies’ scenario, GDP losses of 30 per cent losses are foreseen by 2100. While this may sound a lot, the NGFS group of central banks and supervisors says this is not catastrophic but instead shows how climate change would gradually diminish long-term growth.

Under the NGFS ‘Current Policies’ scenario, GDP losses of 30 per cent losses are foreseen by 2100. While this may sound a lot, the NGFS group of central banks and supervisors says this is not catastrophic but instead shows how climate change would gradually diminish long-term growth.

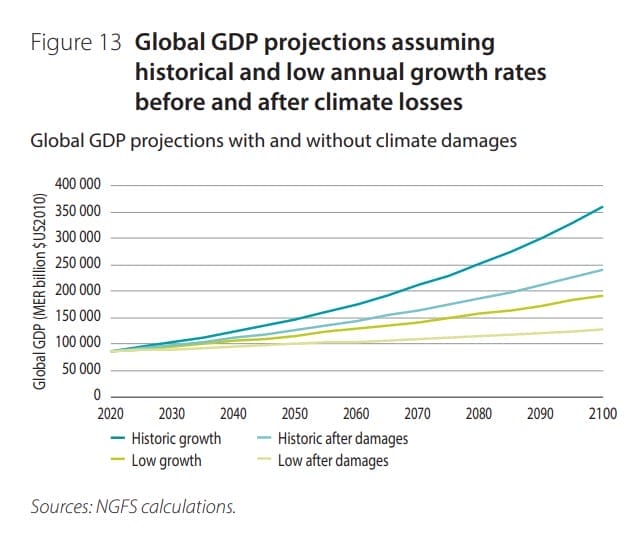

Assuming historical growth rates (1.8 per cent per year) the global economy would grow by more than 300 per cent (i.e. more than quadrupling in size) by the end of the century (see Figure 13). Even after accounting for 30 per cent damage, the global economy would still grow by 180 per cent, NGFS says.

And even assuming more conservative growth of 1 per cent per year, the global economy would still grow by more than 120 per cent after damages.

And even assuming more conservative growth of 1 per cent per year, the global economy would still grow by more than 120 per cent after damages.

Wealth and welfare

NGFS goes on to claim this shows “non-climatic drivers of growth, such as technological innovation, happen to be much more important determinants of future levels of wealth than climate change, even under the new – more severe – damage function”.

It was probably not NGFS’ intention but this statement could be interpreted as suggesting everyone’s ‘wealth’ could still steadily increase even in a 3°C warming world.

Elsewhere, NGFS says “emission reduction is not the end goal of climate action, but rather a means to an end. What climate action actually aims to achieve is to optimise long-term global welfare”.

It is possible that NGFS has its wires crossed and thinks our ‘wealth’ (GDP growth) and ‘welfare’ are the same thing.

NGFS does in fact highlight one other way its paper could be misinterpreted, and stresses that “high climate losses are not an alternative to climate action”.

Higher damages mean less economic growth, and less economic growth means lower emissions. So high-damage NGFS scenarios “may be seen to achieve some emission reductions (although certainly not enough to reach net zero targets) without the corresponding transition risks” that occur in low-emission scenarios such as Net Zero 2050.

But NGFS says “plainly, slowing climate change should not be achieved through physical destruction. Hence, interpreting emission reductions due to climate damages as a societal win would be erroneous”.

Adaptation and resilience

The Investor Group of Climate Change (IGCC) argues in a new report, Activating Private Investment in Adaptation, that Australia needs to significantly scale up investment in adaptation and resilience.

First, to build an investment case for adaptation, IGCC says investors must quantify the financial implications of physical risks to their assets and operations, including indirect impacts via value chain exposures.

However, to do this investors need to rely on climate risk assessments and modelling. But whose modelling do you choose given there are so many open-source and proprietary tools on offer? Is a particular methodology scientifically rigorous and is there transparency about the uncertainties in its projections and predictions?

IGCC says when seeking climate-related data for physical climate risk assessments, investors should look at asset-level geographic – but this can be difficult to obtain.

Even if investors can make the investment case for adaptation, IGGC says, “they will only realise the full financial benefits if valuation standards mature to recognise the higher risk-adjusted returns from climate-resilient assets and businesses. This will unlikely change until evidence-based resilience outcomes are developed”.

Also, even if an individual asset is resilient, this resilience may be undermined if the broader system lacks resilience.

“Investors’ fiduciary duty to invest in the long-term best interests of their beneficiaries is widely interpreted as a duty to maximise portfolio returns, which rules out investments with uncompetitive risk-return profiles.

“Investors are wary of investing in climate resilience as they may not be able to demonstrate the financial benefits, capture them through increased valuation, or access them through the benefit of shared resilience,” according to IGCC.

No time to NAP

IGCC makes recommendations about how the Australian Government can help address these issues.

The National Adaptation Plan (NAP) “should be on-par, in impact and prominence, with the Net Zero Plan. It should include a ‘Net Zero by 2050’ equivalent objective for physical risk.

“As quickly as possible, the NAP should include sector-by-sector plans for adaptation, matching the Net Zero sectoral emissions reduction plans, which are currently in development”.

Sectoral resilience plans would require the Government to set a resilience goal (i.e., a physical risk appetite) and a plan to reach this goal for each sector, according to the paper.

IGCC says private investors, including Australia’s $3.9 trillion superannuation sector, could be a source of adaptation and resilience funding but there was a “considerable risk” of the opposite happening.

“If the free market is left to its own devices, climate change will make it financially rational for private capital to become less available for essential infrastructure and services in regions and industries with more exposure to climate damage and disruption”.

Leave a Comment

You must be logged in to post a comment.