In most cases, the adage “time in the market beats timing the markets” would serve super funds which receive regular contributions and have long investment horizons well. But time is the one thing the $37 billion closed-end State Super does not have.

The NSW public-sector fund is in net outflow. Every five to seven years, it will lose half its size – this is its so-called half-life. Since members are withdrawing money all the time, one of the fund’s primary missions in controlling volatility and making sure there are not massive drawdowns in the portfolio.

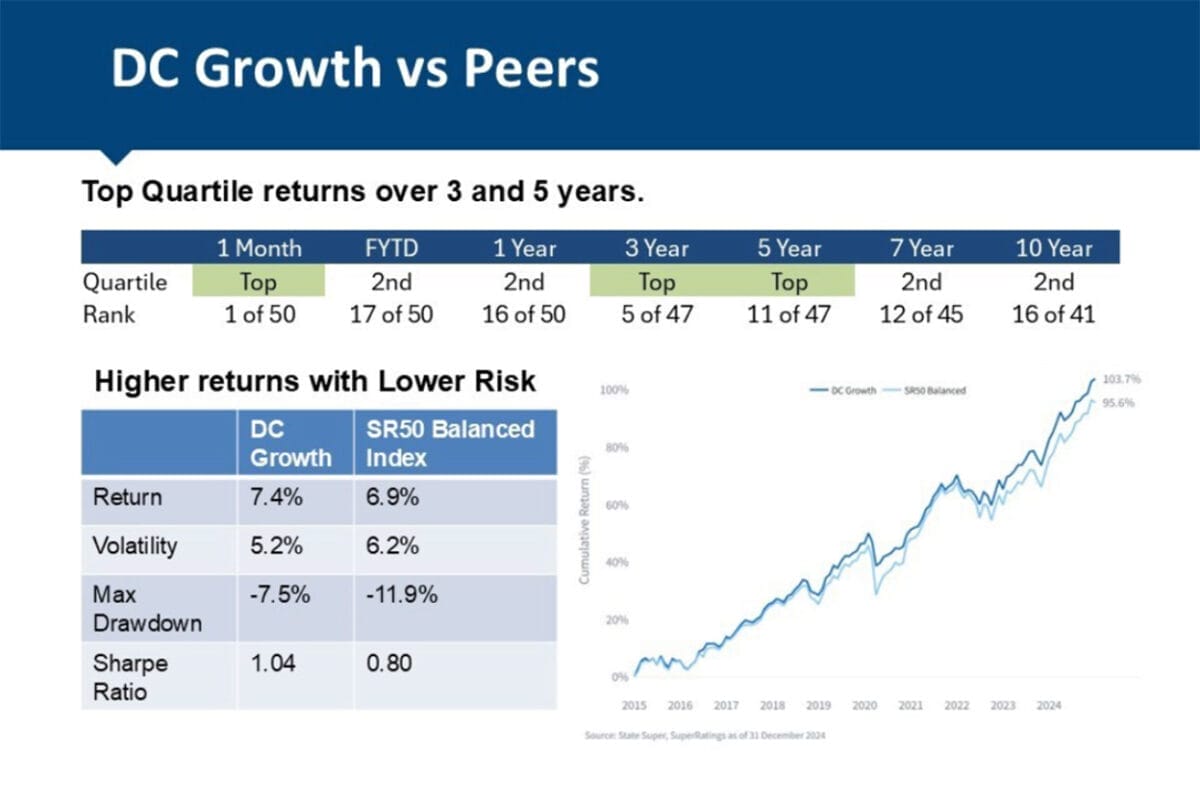

And according to State Super’s own numbers, having below-median volatility has actually delivered above-median returns. The fund’s DC Growth option returned 7.4 per cent per annum over the past decade, while the median fund in SuperRatings’ SR50 Balanced Index delivered 6.9 per cent. But State Super had only a 5.2 per cent standard deviation compared to the median fund’s 6.3 per cent during the period.

CEO of State Super John Livanas says the fund has a three-pronged method to keep volatility in check. The most obvious one is diversification, but he says “one needs to be really careful about what that means”.

“In many cases, diversification is diversification of the price you see,” he tells Investment Magazine. “You may get an infrastructure asset, it gets priced once a month or once a quarter, and now you think you’ve got low volatility when actually you don’t. You just don’t know about the volatility.”

“Diversification is not infrequently priced assets. Diversification is genuinely different factors of risk.”

Staying alert

The second method is through derivatives where, for example, the fund can create put options to protect downside risks. “Of course, the argument is if you do that, you will then have a premium which you’re paying away,” Livanas says.

“[But if] I’m reducing my downside, that means I can take more risk. So if you take more risk to pay for the premium, you can shift – not always – but you can shift the way that the actual investment performs.”

The last one, which Livanas says is probably “the most controversial”, is active portfolio management – things like more frequently moving the risks of the portfolio around, shifting between equities and bonds, extending or shortening the duration, and adding derivatives.

“It’s good to be able to say ‘I don’t want to time the market [when you do have time to be in the market],” he says. “But if you don’t have the time, then you have to do everything in your power to make sure you don’t lose money, and you’re in and out of the market all the time.”

“We need to be in a position where, when we think something is going to happen, we actually have the capacity to move money around, and we do that through effectively derivatives.”

This is combined with another important premise which is being able to capture and understand as much information as possible. State Super has leaned heavily into machine learning models, which track approximately 1600 data points such as currency correlation and alert the investment team of abnormalities. This helps keep the amount of data analysis humans need to do manageable, Livanas says, and sends signals to the investment team when portfolio adjustments need to be made.

Different philosophy

This focus on ensuring smoother returns has shaped State Super’s portfolio in several ways. One is how it works with active managers, who need to meet the payoff timeframe of three to five years or they cannot be considered, Livanas says.

“About half the portfolio will be in active managers, and half won’t be because you just don’t get the payoff,” he says.

“When we sell out of our portfolios, which effectively is constantly rebalancing into less active managers, we’ll use things like smart beta. But active managers do take a bit of time.”

The other impact is State Super’s low volatility and high liquidity need means its investable universe is smaller, which Livanas admits does become a challenge at times.

The fund just sold a combined majority stake in Queensland Airport Limited last year alongside Macquarie Asset Management’s Infrastructure Fund and Australian Retirement Trust, which is State Super’s last infrastructure asset in the DC portfolio. It still holds several local and overseas real assets in the defined benefits portfolio including the parent company of Melbourne Airport and Launceston Airport, but is planning to reduce its private investments progressively in the next two decades.

Pulling out of private markets makes the job harder because “you then don’t have the capacity to actually run volatility through,” he says.

“The DB fund is much steadier, because what comes out of the DB fund is pensions. What comes out of the DC fund is lump sum,” Livanas says. “Pensions are much easier to manage, because you know what the time horizon is going to be, and you’ve got 5 or 10 years before you have to sell an asset.”

“Lots of managers come in with ideas, and I can hear the guys from time to time saying ‘Well that’s very interesting, when and how can I sell it?’ And the manager says ‘What do you mean? You haven’t even bought it yet.’

“But you got to understand that when we buy an asset, we want to know when we’re going to sell it, at what time and who to.”

For this reason, State Super finds pre-IPO strategies attractive as it’s easy to predict exit time and credit funds if they have ample liquidity.

Not for everyone

With that said, Livanas acknowledges whether volatility is a bad thing in a portfolio depends on a fund’s flow profile and investment time horizon. A lot more DC funds are conscious about lowering volatility as a larger proportion of their membership heads into retirement, he says, but it is a different case for those still blessed with net inflow.

“In fact, if anything, you want to actually bias the portfolio to taking more volatility all the way through,” he says.

“The more volatile it is, the more chance you have of buying the dips.”

Volatility has been used as a proxy for risk since the emergence of modern portfolio theory, but the two are not the same concept, Livanas says.

“We should accept volatility and minimise risk, always. And in our case, we need to minimise volatility as well.”

Leave a Comment

You must be logged in to post a comment.