Many Australian investors, including the large superannuation funds, are allocating assets to private markets such as private equity, unlisted infrastructure and private debt. In the right structure, private markets have positively contributed to portfolio return outcomes. However, financial advisers often cite liquidity and transparency of the underlying investments as the biggest challenge to allocating more to private markets. But is it the Australian retail platform infrastructure that constrains advisers from allocating private assets to client portfolios? Or is liquidity more crucial for investor needs when constructing portfolios for the retirement income phase?

Funds currently support large allocations to private markets

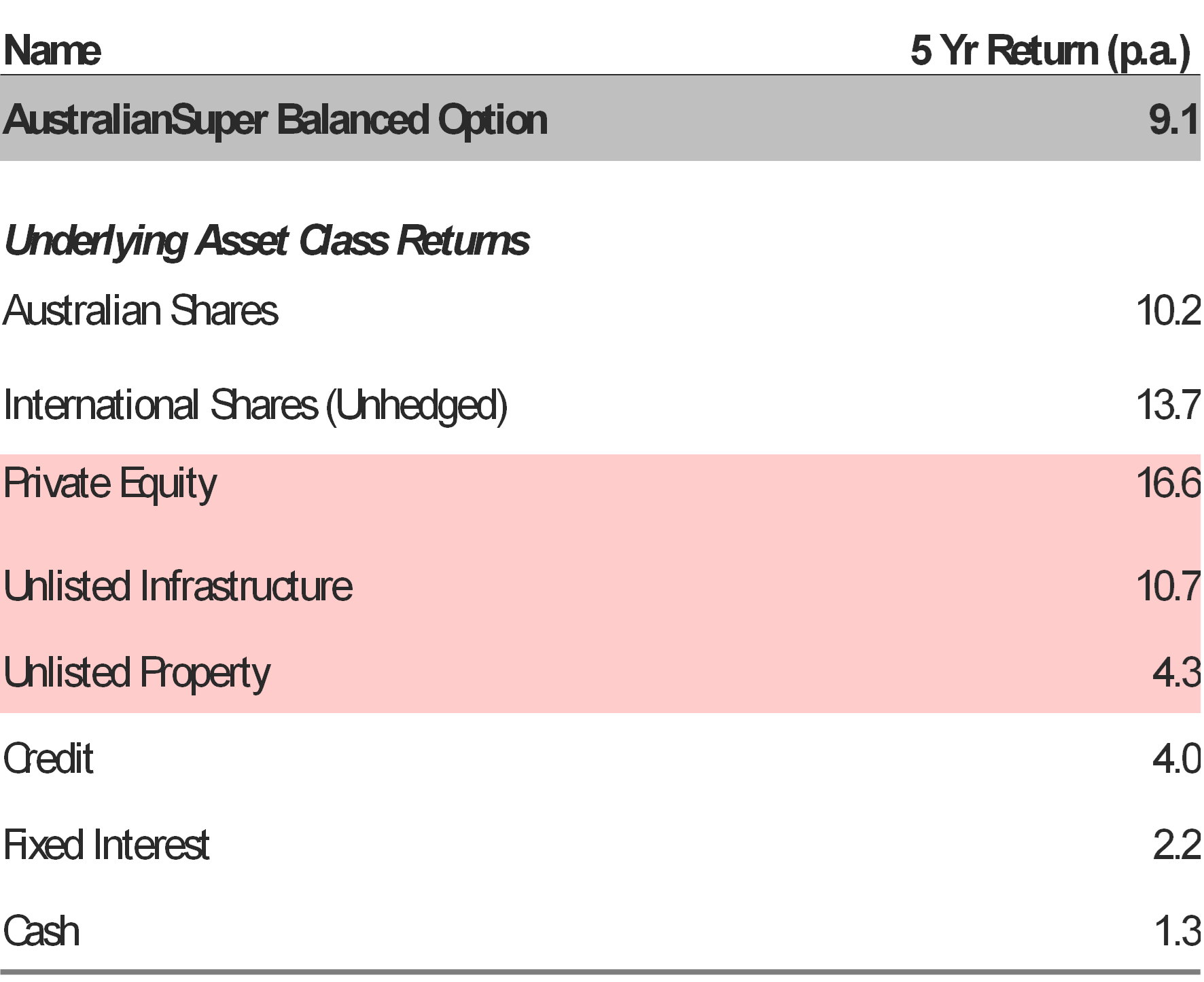

According to APRA, MySuper funds allocated approximately 20% of assets to private equity, unlisted property and unlisted infrastructure (at 31 Dec 2021). It is no secret that some superannuation funds have benefited from holding allocations to private markets. For example, Exhibit 1 shows that AustralianSuper’s Balanced Option enjoyed positive performance contributions from these asset classes over the past five years. But AustralianSuper’s current operational “structure” is largely favourable when it comes to private markets.

AustralianSuper has a very long-term investment horizon; its asset size means it can make large capital outlays, that often affords them a controlling stake in a direct asset; and importantly AustralianSuper is in net inflow with the majority of members accumulating assets rather than drawing a pension. It also has investment teams, processes, and governance structures that are considered appropriate to manage private assets.

Annualised return contribution of AustralianSuper’s Balanced Option (five-year period at 31 March 2022)

Source: AustralianSuper; Asset class returns are AustralianSuper investment returns are based on crediting rates. For super (accumulation) products, crediting rates are returns less investment fees, the percentage-based administration fee that is deducted from returns and taxes. Investment returns aren’t guaranteed. Past performance isn’t a reliable indicator of future returns. Asset Class returns are net of investment management fees and gross of tax. International Equities returns are unhedged.

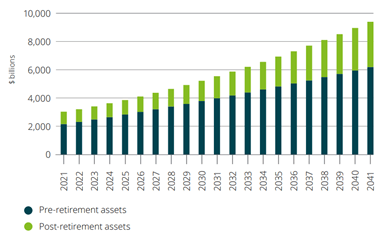

Projection of the mix between pre- and post-retirement assets

Is there a practical solution?

A mismatch of liquidity expectations is always a recipe for disaster. There have been countless examples of less-liquid assets being inappropriately jammed into seemingly liquid product structures and investors lose out with product freezes at times of market volatility. However, listed investment companies could be one possible solution to house these assets as they are closed-ended vehicles and also trade on exchanges. Pinnacle Investment Management recently highlighted the shift in the UK LIC market over the last two decades towards infrastructure, property, and private equity to try to solve this issue.

However, the experience in Australia where some LICs trade at persistent discounts to net asset value could dampen investor adoption or result in poor outcomes if investor behaviour is not well managed.

The cogs of innovation continue to turn—tokenisation and fractionalisation could eventually benefit investors, but product innovation here remains nascent. In the meantime, it’s worth considering whether some superannuation funds with the “right structures”—that is, larger allocations to private markets and well-managed liquidity—could provide an appropriate access point to private markets for some clients, at least until they face the looming challenge of managing a greater proportion of fund assets for the post-retirement phase

Leave a Comment

You must be logged in to post a comment.